US Labour Market Collapse Sets Stage for Aggressive Fed Easing | Links: [1], [2], [3]

The US labour market has suffered its most dramatic deterioration since the pandemic recovery began, with private sector hiring collapsing to just 54,000 jobs in August according to ADP data. This represents a stark escalation beyond the gradual softening that initially prompted Fed dovish signals, now coupled with initial jobless claims rising to four-month highs. The data shock has fundamentally altered the Fed's policy calculus, with NY Fed President Williams reinforcing the urgent pivot by stating it's "appropriate to cut rates over time." Treasury markets are positioning aggressively ahead of Friday's official payrolls data, with unemployment expected to rise further and wage growth moderating across the breadth of the labour market.

Trump Threatens Semiconductor Tariffs While Protecting Apple | Links: [4], [5], [6]

President Trump announced "fairly substantial" tariffs on semiconductor imports coming "shortly," targeting firms that refuse to move production to the US while explicitly signalling protection for Apple and other major tech companies maintaining close White House relationships. The selective enforcement approach emerged from a White House tech dinner where companies pledged increased AI spending, demonstrating the administration's carrot-and-stick strategy. The policy aims to force global chipmakers to establish US manufacturing facilities, fundamentally reshaping semiconductor supply chains optimised around Asian production for decades. This comes as Trump hosts tech leaders willing to increase domestic investment, creating a bifurcated landscape where foreign chip producers face substantial tariffs whilst US-aligned companies benefit from preferential treatment.

Japanese Wage Growth Strengthens BOJ Rate Hike Case | Links: [7], [8]

Japanese wages gained the most in seven months in July, with real wages turning positive for the first time since December 2023, significantly strengthening the case for Bank of Japan interest rate increases. This development marks a potential end to decades of deflation concerns as domestic demand shows recovery signs and service sector inflation remains elevated. BOJ Governor Ueda's recent hawkish comments gain credibility with this wage data, suggesting the central bank may accelerate normalisation beyond current market expectations. The wage growth acceleration represents a fundamental shift in Japan's economic dynamics, with sustainable wage-price spiral conditions potentially emerging for the first time in a generation.

Global Bond Rout Intensifies as Central Bank Independence Under Attack | Links: [9], [10], [11], [12]

Global fixed income markets are experiencing widespread selling pressure, with UK gilt yields hitting 27-year highs as investors dump government debt across major markets amid escalating central bank independence concerns. The selloff has intensified beyond previous episodes as Trump's renewed attempts to remove Fed Governor Lisa Cook create unprecedented governance anxieties affecting global monetary policy credibility. Bank of England Governor Andrew Bailey's warning that the Fed is going down a "dangerous road" highlights institutional crisis risks that now compound traditional fiscal sustainability concerns. Goldman Sachs' projection that gold could reach $5,000 if Fed independence is compromised signals potential dollar reserve currency risks, representing a qualitative escalation from previous political pressure episodes that is fundamentally repricing sovereign debt globally.

Asset Management Giants Consolidate as Private Markets Democratise | Links: [13], [14]

Goldman Sachs is investing $1 billion in T. Rowe Price as part of a strategic partnership to democratise private market access for retail investors, marking a fundamental shift in asset management industry structure. The landmark transaction aims to provide broader investor access to private equity, credit, and real estate investments historically limited to institutions, with T. Rowe Price shares surging on the announcement. This reflects growing demand for alternative investments amid low traditional fixed income yields and validates the strategic rationale for partnerships that blur traditional boundaries between investment banking and asset management. The trend suggests asset managers are leveraging strategic alliances to compete with private equity firms increasingly moving into traditional territory, potentially accelerating sector consolidation as alternatives become mainstream portfolio components.

| Dow Jones Industrial Average | --▲ +0.92% |

| S&P 500 | --▲ +0.70% |

| Hang Seng Index | --▼ -1.69% |

| FTSE 100 | --▲ +0.42% |

| CAC 40 | --▼ -0.03% |

| DAX 40 | --▲ +0.45% |

| Euro Stoxx 50 | --▲ +0.37% |

| Nasdaq Composite | --▲ +0.78% |

| Nasdaq-100 | --▲ +0.81% |

| Nikkei 225 | --▲ +1.16% |

| S&P/ASX 200 | --▲ +1.00% |

| Shanghai Composite | --▼ -1.10% |

• UK Retail Sales MoM at 07:00 BST - Forecast: 0.5% vs Previous: 0.9% - Key gauge of consumer spending strength that will influence BoE policy decisions and GBP direction.

• Canadian Unemployment Rate at 13:30 BST - Previous: 6.9% - Critical labour market indicator that will shape Bank of Canada monetary policy expectations and CAD volatility.

• US Non Farm Payrolls at 13:30 BST - Previous: 73.0K - The most watched US jobs report that drives Federal Reserve policy expectations and major USD movements across all markets.

• US Unemployment Rate at 13:30 BST - Previous: 4.2% - Complementary labour market data that reinforces Fed policy direction and impacts Treasury yields and equity sentiment.

• Canadian Ivey PMI s.a at 15:00 BST - Previous: 55.8 - Leading business sentiment indicator that signals economic momentum and influences CAD and commodity-linked assets.

No major earnings events scheduled for today.

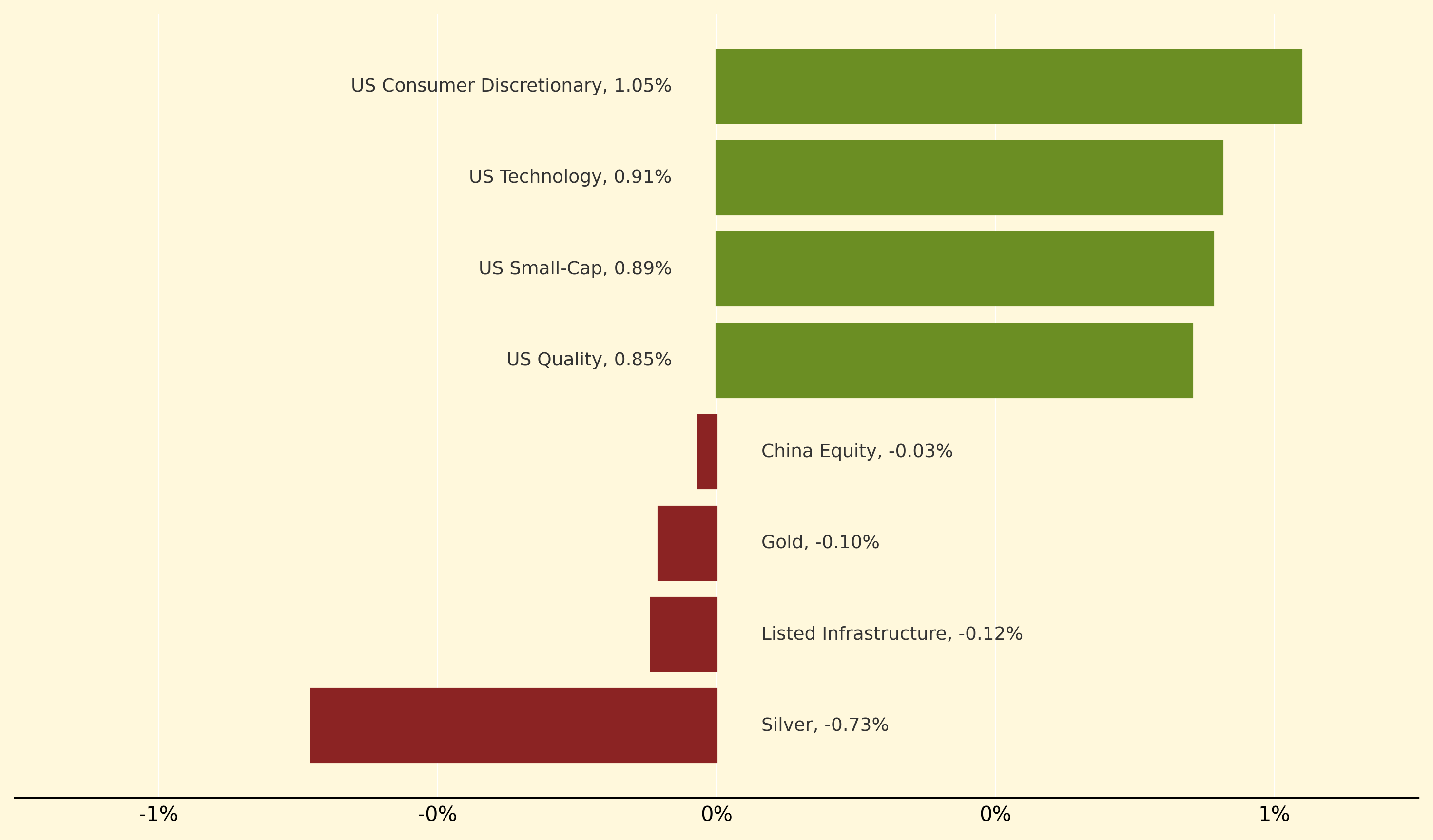

US Consumer Discretionary led yesterday's gains, climbing 1.05% as markets positioned ahead of critical jobs data, whilst US Technology advanced 0.91% despite Trump's announced semiconductor tariffs targeting foreign producers. US Small-Cap strategies also performed well, rising 0.89%, benefiting from expectations of aggressive Fed easing following the dramatic deterioration in private sector hiring to just 54,000 jobs in August.

Precious metals underperformed significantly, with Silver dropping 0.73% and Gold falling 0.10% as global fixed income market turmoil intensified amid central bank independence concerns. Listed Infrastructure also lagged, declining 0.12%, whilst China Equity remained flat at -0.03% as the world-beating rally showed signs of cooling despite policy meeting speculation.

Wage-price spiral: A self-reinforcing cycle where rising wages drive higher prices, which then prompt workers to demand further wage increases. This dynamic is particularly significant for central banks as it can entrench inflation expectations and make price stability harder to achieve without aggressive monetary tightening.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry