Powell's December Caution Creates Fed Policy Uncertainty Despite Rate Cut | Links: [1], [2], [3], [4]

The Federal Reserve delivered its anticipated 25 basis point cut yesterday, lowering rates to 4.50-4.75%, yet Chair Powell's cautious rhetoric triggered significant bond market volatility. His measured warning that December rate cuts remain "far from assured" caused market expectations to plummet from 90% to 71% overnight. The decision revealed considerable divisions within the FOMC, with Governor Miran dissenting for a larger 50bp cut whilst Governor Schmid opposed any easing entirely. Powell's hawkish tone coincided with the Fed's announcement to conclude balance sheet runoff in December and potentially expand holdings again—a complex signal indicating policy uncertainty ahead. The 10-year Treasury yield surged back above 4% whilst the dollar strengthened across major pairs.

Nvidia Achieves $5 Trillion Milestone as AI Infrastructure Investment Validates Megacap Concentration | Links: [5], [6], [7]

History was made as Nvidia became the first company ever to exceed the $5 trillion market capitalisation threshold, completing an extraordinary 1087% rise since ChatGPT's launch. The milestone reflects sustained investor confidence in AI infrastructure demand, though it amplifies concerns about dangerous market concentration in a single stock. Big Tech earnings delivered mixed signals on AI spending sustainability—Microsoft's record $35 billion quarterly capex raised efficiency questions despite 40% Azure growth, whilst Meta absorbed a $16 billion tax charge that offset solid operational performance. Alphabet crossed $100 billion in quarterly revenue for the first time with cloud growing 34%, though the overarching question remains whether these massive capital deployments can generate proportional returns. The AI investment thesis holds for now, but scrutiny over spending efficiency continues mounting.

Trump-Xi Summit Produces Trade War Truce with Chinese Tariff Reductions to 47% | Links: [8], [9], [10]

The closely monitored 90-minute Trump-Xi bilateral meeting in South Korea concluded with trade concessions that surpassed market expectations. Trump announced tariff reductions on Chinese goods to 47% whilst securing agreements on rare earth exports and what he characterised as "tremendous" soybean purchases from Beijing. The breakthrough featured Xi adopting a notably conciliatory approach, referring to the two nations as "partners and friends"—language suggesting a tactical pause in trade hostilities. However, concrete details remain limited, with Trump expecting formal agreements to be signed Thursday. This development comes as China's manufacturing sector endures its seventh consecutive month of contraction and growing pressure from US allies to diversify supply chains, making the timing crucial for both economies.

Trump Orders Nuclear Testing Resumption as Geopolitical Tensions Rise | Links: [11]

President Trump directed the U.S. to restart nuclear weapons testing, citing rival nations' programmes in a fundamental shift that breaks decades of nuclear testing moratorium. This dramatic escalation in geopolitical posture toward Russia and China's nuclear capabilities could trigger substantial defence spending increases across NATO allies and destabilise existing arms control agreements. The announcement adds another volatile layer to already elevated global tensions from trade negotiations and territorial disputes. Defence contractors and nuclear technology companies stand as likely beneficiaries, whilst the move risks prompting reciprocal responses from other nuclear powers and fundamentally reshaping the global security landscape. Markets will now need to price in heightened geopolitical risk premiums alongside traditional economic uncertainties.

Samsung Chip Profits Jump 160% as AI Memory Demand Confirms Semiconductor Supercycle | Links: [12]

Samsung's third-quarter operating profit more than doubled, climbing 160% year-over-year and beating estimates as AI chip demand drove memory sales to record levels. The Korean tech giant's semiconductor division led a remarkable recovery from 2023's brutal industry downturn, with the company aggressively expanding high-bandwidth memory (HBM) production amid supply shortages extending into next year. This positions Samsung alongside SK Hynix as a key beneficiary of the AI infrastructure buildout, providing concrete evidence of the semiconductor supercycle thesis. The results demonstrate genuine monetisation of AI demand across the supply chain and reinforce the structural nature of current technology investment cycles, potentially pressuring other memory manufacturers to accelerate their own capacity expansion plans.

| S&P 500 | 6890.59-20.36▼ -0.29% |

| FTSE 100 | 9756.10+59.30▲ +0.61% |

| CAC 40 | 8200.88+2.17▲ +0.03% |

| DAX 40 | 24124.20-136.90▼ -0.56% |

| Dow Jones | 47632.00-114.80▼ -0.24% |

| Euro Stoxx 50 | 5705.81+4.57▲ +0.08% |

| Nasdaq 100 | 26119.80-27.90▼ -0.11% |

| Nasdaq Comp | 23958.50-28.80▼ -0.12% |

| Nikkei 225 | 51307.60+854.00▲ +1.69% |

| S&P/ASX 200 | 8926.20-86.30▼ -0.96% |

| Shanghai Comp | 4016.33+26.07▲ +0.65% |

| S&P 500 E-mini | 6923.00+0.25▲ +0.00% |

| Nasdaq 100 | 26254.20-8.25▼ -0.03% |

| FTSE 100 | 9755.50-31.50▼ -0.32% |

| Euro Stoxx 50 | 5708.00-2.00▼ -0.04% |

| WTI Crude | 60.17-0.31▼ -0.51% |

| Gold | 3973.80-26.90▼ -0.67% |

| Copper | 5.16-0.11▼ -2.06% |

| US 10Y Treasury | 112.86-0.05▼ -0.04% |

| UK 10Y Gilt | 118.13-0.15▼ -0.13% |

| German 10Y Bund | 129.31-0.26▼ -0.20% |

| Italian 10Y BTP | 121.45+0.10▲ +0.08% |

| US Dollar Index | 98.77-0.19▼ -0.19% |

| VIX Volatility | 18.90-0.03▼ -0.19% |

| SONIA 3M | 96.25-0.01▼ -0.01% |

• French GDP Growth Rate QoQ Prel at 06:30 GMT - Forecast: 0.1% vs Previous: 0.3% - Weaker than expected growth could weigh on EUR and raise concerns about eurozone economic momentum ahead of ECB decision.

• German GDP Growth Rate QoQ Flash at 09:00 GMT - Forecast: 0.0% vs Previous: -0.3% - Any return to positive growth could support EUR strength and influence ECB policy stance on further rate cuts.

• Italian GDP Growth Rate QoQ Adv at 09:00 GMT - Forecast: 0.1% vs Previous: -0.1% - Recovery from contraction would bolster eurozone growth outlook and provide ECB with more policy flexibility.

• EU GDP Growth Rate QoQ Flash at 10:00 GMT - Forecast: 0.1% vs Previous: 0.1% - Sustained modest growth supports ECB's cautious approach to monetary easing and EUR stability.

• US GDP Growth Rate QoQ Adv at 12:30 GMT - Forecast: 3.0% vs Previous: 3.8% - Still-robust growth despite deceleration reinforces Fed's patient approach to rate cuts and supports USD strength.

• German Inflation Rate YoY Prel at 13:00 GMT - Forecast: 2.2% vs Previous: 2.4% - Continued disinflation toward ECB target provides room for potential rate cuts and pressures EUR.

• EU ECB Interest Rate Decision at 13:15 GMT - Forecast: 2.15% vs Previous: 2.15% - Rate hold expected but forward guidance will be crucial for EUR direction amid mixed eurozone data.

• EU ECB Press Conference at 13:45 GMT - Lagarde's commentary on growth outlook and future policy path will drive EUR volatility and European bond markets.

• Shell Plc (SHEL) at 07:00 GMT [Pre-Market] - Est: $0.83 vs Prev: $0.72 - Energy sector earnings with strong surprise could influence broader commodity and European equity sentiment.

• Banco Bilbao Vizcaya Argentaria, S.A. (BBVA) at 07:00 GMT [Pre-Market] - Est: $0.53 vs Prev: $0.54 - European banking results may signal regional financial sector health amid interest rate environment changes.

• Merck & Company, Inc. (MRK) at 10:30 GMT [Pre-Market] - Est: $2.35 vs Prev: $2.13 - Pharmaceutical giant's performance could impact healthcare sector and broader market confidence.

• Eli Lilly and Company (LLY) at 10:45 GMT [Pre-Market] - Est: $5.92 vs Prev: $6.31 - Diabetes and weight-loss drug leader's strong surprise may drive healthcare and growth stock momentum.

• S&P Global Inc. (SPGI) at 11:15 GMT [Pre-Market] - Est: $4.42 vs Prev: $4.43 - Financial data provider's results reflect corporate activity levels and market infrastructure demand.

• Samsung Electronics Co., Ltd. (005930) at 12:00 GMT [Pre-Market] - Est: $0.98 vs Prev: $0.54 - Global semiconductor bellwether's disappointing results could pressure tech sector and Asian markets.

• Mastercard Incorporated (MA) at 13:30 GMT [During-Hours] - Est: $4.32 vs Prev: $4.15 - Payment processor's consumer spending insights crucial for economic sentiment and fintech sector.

• Amazon.com, Inc. (AMZN) at 20:01 GMT [During-Hours] - Est: $1.57 vs Prev: $1.68 - Mega-cap tech leader's strong surprise and cloud guidance will significantly impact market sentiment and tech valuations.

• Apple Inc. (AAPL) at 20:30 GMT [During-Hours] - Est: $1.77 vs Prev: $1.57 - World's largest company by market cap will drive overall market direction and technology sector performance.

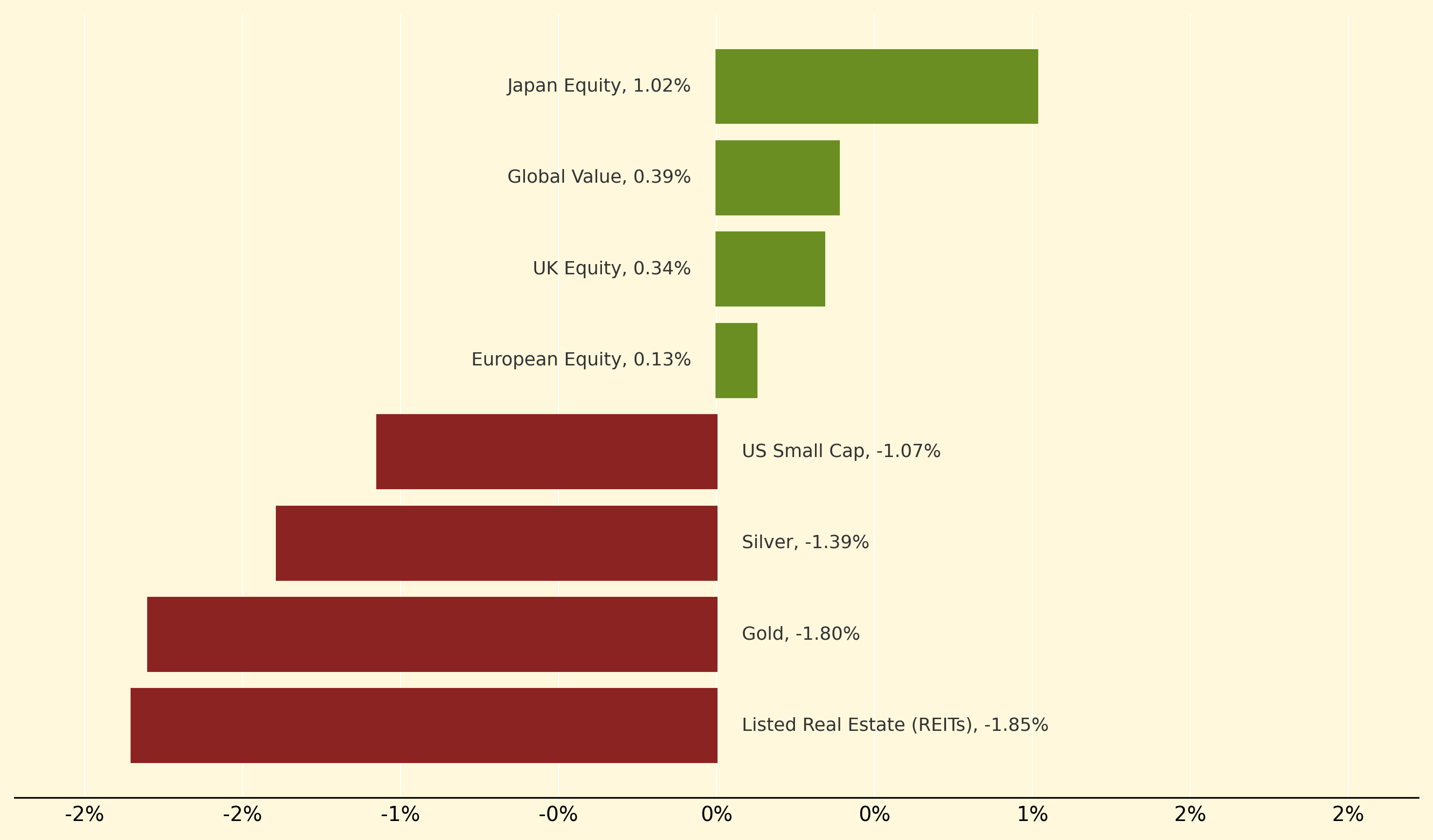

Japan Equity led regional markets with a robust 1.02% gain, capitalising on the Bank of Japan's decision to hold rates steady whilst maintaining future hike optionality. Global Value strategies also advanced well, gaining 0.39%, as investors shifted toward defensive positioning amid Fed policy uncertainty and geopolitical tensions from Trump's nuclear testing announcement.

Listed Real Estate (REITs) experienced the steepest decline at -1.85%, pressured by Powell's hawkish stance that drove 10-year Treasury yields surging back above 4%. Gold fell -1.8% and Silver dropped -1.39% as the strengthening dollar and reduced December rate cut expectations (falling from 90% to 71%) diminished precious metals' appeal as inflation hedges.

Balance sheet runoff: The Federal Reserve's systematic reduction of its bond holdings by allowing maturing securities to roll off without reinvestment, effectively tightening monetary policy by reducing money supply and market liquidity without directly raising interest rates.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry