Fed Operates in Data Blackout as Rate Cut Decision Looms | Links: [1], [2]

The Federal Reserve confronts an unprecedented challenge this week, approaching an expected 25 basis point rate reduction whilst operating in an information vacuum caused by the government shutdown. Critical economic indicators including employment reports, inflation data, and GDP figures remain unavailable precisely as policymakers make essential monetary policy decisions. Markets continue pricing in the rate reduction despite Fed officials lacking fundamental economic intelligence to assess the economy's trajectory. This extraordinary information void creates heightened uncertainty around policy effectiveness, with global implications as other central banks monitor for any communication surprises from a Fed operating essentially blind to current economic conditions.

Australia's Inflation Shock Rules Out RBA Rate Cuts | Links: [3], [4]

Australia delivered a monetary policy bombshell as Q3 inflation accelerated to 1.3% quarterly and 3.2% annually, crushing rate cut expectations and forcing Goldman Sachs to completely reverse their forecasts. Core inflation jumped to 3.0% annually—the highest in over a year—driven by persistent services and food costs that pushed well above the RBA's 2-3% target range. Markets immediately priced out any RBA cuts whilst the Australian dollar strengthened sharply as investors repositioned for an extended pause. This creates stark divergence from the Fed and other major central banks, presenting Governor Michele Bullock with a significant policy challenge as domestic price pressures prove more resilient than anticipated.

US-China Trade Relations Show Tentative Thaw | Links: [5], [6]

President Trump signalled potential progress ahead of his South Korea meeting with Xi Jinping, indicating he expects to lower fentanyl-related tariffs whilst discussing agricultural trade cooperation. China made immediate goodwill gestures through purchases of three US soybean cargoes from the 2024 harvest—their first such purchases of the season—as commodity markets responded with soybeans hitting 15-month highs. Trump's comments about expecting to discuss "farmers" with Xi suggest broader agricultural cooperation beyond the symbolic purchases. The diplomatic positioning comes amid ongoing technology discussions around Nvidia's advanced AI chips, though Trump's continued criticism of Fed Chair Powell adds domestic policy uncertainty to the equation.

FTSE 100 Hits Record High on HSBC Asia Pivot | Links: [7]

The FTSE 100 touched a new all-time peak as HSBC surged 4.6% on CEO Georges Elhedery's successful strategic pivot toward Asian markets, with Q3 results demonstrating strong Hong Kong expansion and healthy 7.2% loan growth metrics. The banking giant's Asian focus provided crucial support to the broader index, whilst the FTSE 250 jumped 4.6% in a demonstration of domestic market momentum. This milestone highlights UK equity resilience despite ongoing fiscal concerns and sterling weakness ahead of November's budget. The performance contrasts sharply with currency headwinds and underscores how international exposure within UK-listed companies provides growth catalysts that domestic economic uncertainty cannot derail.

Corporate Restructuring Wave Signals AI-Driven Transformation | Links: [8], [9], [10]

A sweeping corporate restructuring wave reshapes the global workforce as companies pivot toward AI-driven operations, with over 45,000 positions eliminated this month alone. Amazon announced 14,000 redundancies whilst increasing AI investments, UPS cut 48,000 jobs amid reduced Amazon partnerships, and the reductions predominantly target white-collar roles as automation streamlines operations. Meanwhile, OpenAI completed its for-profit restructuring with Microsoft securing a 27% stake worth $135 billion, exemplifying the capital-intensive nature of AI development. This transformation reflects a fundamental shift in corporate cost structures as companies trade traditional employment models for technology infrastructure, creating near-term economic uncertainty whilst potentially unlocking longer-term productivity gains across industries.

| S&P 500 | 6890.89-6.85▼ -0.10% |

| FTSE 100 | 9696.70+42.90▲ +0.44% |

| CAC 40 | 8216.58-2.95▼ -0.04% |

| DAX 40 | 24278.60+50.40▲ +0.21% |

| Dow Jones | 47706.40-46.00▼ -0.10% |

| Euro Stoxx 50 | 5704.35+8.30▲ +0.15% |

| Hang Seng | 26346.10-162.70▼ -0.61% |

| Nasdaq 100 | 26012.20+79.60▲ +0.31% |

| Nasdaq Comp | 23827.50+61.00▲ +0.26% |

| Nikkei 225 | 50219.20-137.90▼ -0.27% |

| S&P/ASX 200 | 9012.50-43.10▼ -0.48% |

| Shanghai Comp | 3988.22+1.33▲ +0.03% |

| S&P 500 E-mini | 6939.75+14.00▲ +0.20% |

| Nasdaq 100 | 26252.20+88.75▲ +0.34% |

| FTSE 100 | 9735.00-1.50▼ -0.02% |

| Euro Stoxx 50 | 5700.00-9.00▼ -0.16% |

| WTI Crude | 60.07-0.08▼ -0.13% |

| Gold | 3972.10-11.00▼ -0.28% |

| Copper | 5.17+0.00▲ +0.08% |

| US 10Y Treasury | 113.45-0.02▼ -0.01% |

| UK 10Y Gilt | 118.29+0.02▲ +0.02% |

| German 10Y Bund | 129.54-0.03▼ -0.02% |

| Italian 10Y BTP | 121.35-0.01▼ -0.01% |

| US Dollar Index | 98.67+0.15▲ +0.15% |

| VIX Volatility | 18.42-0.16▼ -0.82% |

| SONIA 3M | 96.25+0.01▲ +0.02% |

• UK BoE Consumer Credit at 09:30 GMT - Previous: 1.692 - Provides insight into UK household borrowing trends and consumer spending capacity ahead of holiday season.

• US Goods Trade Balance Adv at 12:30 GMT - Forecast: -90.0 vs Previous: -85.5 - Wider deficit could pressure USD and influence Fed policy considerations on economic growth.

• Canada BoC Interest Rate Decision at 13:45 GMT - Forecast: 2.25% vs Previous: 2.50% - Expected 25bps cut could weaken CAD and signal dovish shift in North American monetary policy.

• Canada BoC Monetary Policy Report at 13:45 GMT - Key forward guidance on inflation outlook and economic projections will shape CAD and bond market expectations.

• Canada BoC Press Conference at 14:30 GMT - Governor Macklem's commentary on rate path and economic conditions will drive CAD volatility and market positioning.

• US Fed Interest Rate Decision at 18:00 GMT - Forecast: 4.00% vs Previous: 4.25% - Anticipated 25bps cut will impact USD strength and global risk sentiment across equity and bond markets.

• US Fed Press Conference at 18:30 GMT - Powell's guidance on 2025 rate path and economic outlook will be crucial for USD direction and global market positioning.

• Caterpillar, Inc. (CAT) at 10:30 GMT [Pre-Market] - Est: $4.53 vs Prev: $4.72 - Industrial bellwether's results will signal global infrastructure demand and economic momentum across key markets.

• Verizon Communications Inc. (VZ) at 10:30 GMT [Pre-Market] - Est: $1.19 vs Prev: $1.22 - Telecom giant's subscriber growth and 5G investment returns will indicate consumer spending resilience and tech infrastructure health.

• Boeing Company (The) (BA) at 11:30 GMT [Pre-Market] - Est: $-5.16 vs Prev: $-1.24 - Aerospace recovery trajectory and production ramp-up guidance will impact broader industrial and travel sector sentiment.

• SK hynix Inc. (000660) at 12:00 GMT [Pre-Market] - Est: $8.88 vs Prev: $7.05 - Memory chip demand outlook will drive semiconductor sector direction and AI infrastructure investment themes.

• Bank of China Limited Class A (601988) at 12:00 GMT [Pre-Market] - Est: $0.03 vs Prev: $0.03 - Major Chinese bank's results will reflect domestic economic health and credit demand in the world's second-largest economy.

• Airbus SE (AIR) at 12:00 GMT [Pre-Market] - Est: $1.91 vs Prev: $1.74 - European aerospace leader's delivery guidance will signal aviation recovery strength and supply chain normalisation.

• UBS Group AG (UBSG) at 12:00 GMT [Pre-Market] - Est: $0.49 vs Prev: $0.72 - Wealth management performance will indicate high-net-worth client activity and European banking sector health.

• Automatic Data Processing, Inc. (ADP) at 13:30 GMT [During-Hours] - Est: $2.44 vs Prev: $2.26 - Payroll processor's results serve as a real-time barometer of US employment trends and business hiring confidence.

• Microsoft Corporation (MSFT) at 20:00 GMT [During-Hours] - Est: $3.67 vs Prev: $3.65 - Cloud computing and AI revenue growth will set tone for mega-cap tech valuations and enterprise spending trends.

• Alphabet Inc. (GOOG) at 20:00 GMT [During-Hours] - Est: $2.27 vs Prev: $2.31 - Search advertising strength and AI investment returns will drive broader digital advertising and tech sector sentiment.

• Meta Platforms, Inc. (META) at 20:00 GMT [During-Hours] - Est: $6.72 vs Prev: $7.14 - Social media advertising resilience and metaverse spending will influence consumer discretionary and tech growth expectations.

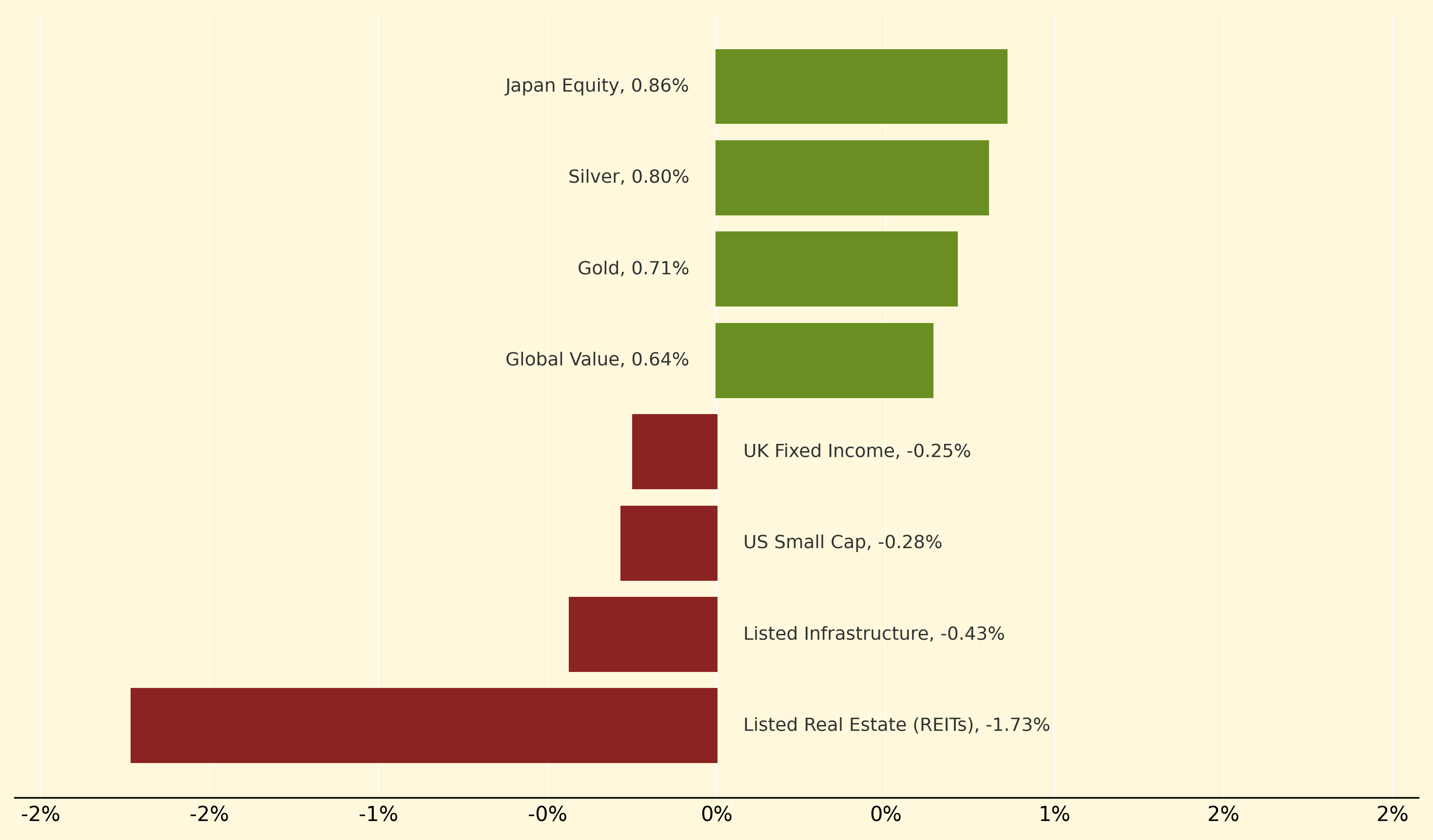

Japanese equities topped gains at 0.86% as the Nikkei crossed 51,000 for the first time, driven by technology optimism and Tokyo-Washington trade cooperation expectations ahead of the Trump-Xi meeting. Precious metals also performed strongly, with silver advancing 0.8% and gold climbing 0.71% as investors positioned defensively amid Fed rate cut uncertainty and the central bank's information vacuum ahead of this week's policy decision.

Listed Real Estate (REITs) suffered the steepest decline at -1.73%, reflecting rate-sensitive sector weakness as markets priced in potential Fed policy surprises despite expected cuts. Infrastructure assets also lagged at -0.43%, whilst US Small Cap fell -0.28% as corporate restructuring waves and AI-driven workforce changes created uncertainty around domestic growth prospects amid the broader economic data shortage facing policymakers.

data blackout: A period when government shutdowns prevent the release of critical economic statistics that central banks rely on for monetary policy decisions, forcing policymakers to operate without essential real-time intelligence on employment, inflation, and GDP trends.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry