Fed Independence Under Siege as Rate Cut Week Begins | Links: [1], [2], [3]

The Federal Reserve enters its September meeting facing unprecedented political interference as Trump attempts to reshape monetary policy through board appointments and public pressure. Appeals courts blocked Trump's effort to dismiss Governor Lisa Cook before the meeting, whilst Stephen Miran's confirmation to the Fed Board, despite maintaining his White House role, creates potential conflicts of interest at the heart of global dollar policy. Trump's public calls for "bigger" rate cuts and his criticism of the Fed represent a fundamental challenge to central bank autonomy. Markets have fully priced 25-50 basis points of cuts, but the political drama surrounding the institution responsible for global monetary policy creates uncertainty that extends beyond Wednesday's rate decision.

Global Markets Hit Records Amid Dollar Retreat and Gold Rally | Links: [4], [5], [6]

Equity markets across the globe scaled fresh records as the S&P 500 breached 6,600 for the first time and Asian indices reached multi-year highs, driven by Fed easing expectations. The dollar weakened broadly against major currencies as traders positioned for 67 basis points of rate cuts by year-end, whilst gold hit new all-time highs near $3,700 with Goldman Sachs targeting $4,000. Alphabet joined the $3 trillion market cap club and Tesla surged on Elon Musk's $1 billion stock purchase. The synchronised global rally demonstrates how Fed policy transmission affects every major asset class, creating both opportunity and concentration risk as valuations stretch further into uncharted territory.

BIS Warns Market Rally Conceals Deep Economic Cracks | Links: [7], [8], [9]

The Bank for International Settlements issued a stark warning that the current market euphoria is masking fundamental economic weaknesses and growing disconnects between equity and debt markets. The central bank umbrella organisation flagged elevated asset valuations, mounting fiscal sustainability concerns, and potential amplification channels that could trigger broader corrections. The BIS noted that any significant portfolio shift away from US assets would likely be gradual, but warned of systemic risks building beneath record market highs.

US-China Tech Tensions Escalate Despite Trade Progress | Links: [10], [11], [12]

China's antitrust investigation found that Nvidia violated monopoly laws, escalating tensions as US-China trade talks show progress on TikTok. The preliminary probe targets Nvidia's 2020 Mellanox acquisition and occurs just one day after Treasury Secretary Bessent announced a TikTok deal framework, evidencing the multi-layered nature of US-China economic relations, where trade negotiations can advance whilst technology competition intensifies. The divergent trajectories suggest that any broader economic détente will remain fragmented across industries.

Energy Sector Faces Structural Investment Challenge | Links: [13], [14]

The IEA warns that accelerating global oil field decline rates means that 90% of upstream investment is used just to offset existing production losses, with companies collectively spending $500 billion annually "to stand still." This structural challenge coincides with BP's major Brazilian oil discovery, signalling renewed exploration appetite despite ESG pressures, whilst Ukrainian attacks on Russian energy facilities could lead to immediate supply issues. The convergence of declining field productivity, capital intensity increases, and supply disruptions continues the complex investment environment where energy companies must balance immediate security concerns with long-term transition pressures.

| Dow Jones Industrial Average | --▲ +0.08% |

| S&P 500 | --▲ +0.18% |

| Hang Seng Index | --▲ +0.52% |

| FTSE 100 | --▼ -0.07% |

| CAC 40 | --▲ +0.62% |

| DAX 40 | --▼ -0.15% |

| Euro Stoxx 50 | --▲ +0.69% |

| Nasdaq Composite | --▲ +0.47% |

| Nasdaq-100 | --▲ +0.48% |

| S&P/ASX 200 | --▼ -0.13% |

| Shanghai Composite | --▼ -0.40% |

| S&P 500 E-mini | 6684.75+5.50▲ +0.08% |

| Nasdaq-100 | 24583.50+32.75▲ +0.13% |

| FTSE 100 Index | 9288.50+7.00▲ +0.08% |

| EURO STOXX 50 | 5444.00+4.00▲ +0.07% |

| WTI Crude Oil | 63.39+0.09▲ +0.14% |

| Gold (COMEX) | 3721.20+2.20▲ +0.06% |

| Copper (COMEX) | 4.69-0.03▼ -0.68% |

| US 10-Year Treasury | 113.45-0.02▼ -0.01% |

| UK Long Gilt (10Y) | 117.85-0.05▼ -0.04% |

| German Bund (10Y) | 128.71-0.02▼ -0.02% |

| Italian BTP (10Y) | 120.26+0.34▲ +0.28% |

| US Dollar Index | 96.81-0.15▼ -0.16% |

| VIX Volatility | 18.15+0.01▲ +0.07% |

| SONIA 3M Interest Rate | 96.03+0.01▲ +0.01% |

• UK Unemployment Rate at 07:00 BST - Forecast: 4.7% vs Actual: 4.7% - Key indicator for Bank of England policy decisions and broader economic health assessment.

• German ZEW Economic Sentiment Index at 10:00 BST - Forecast: 25.0 vs Previous: 34.7 - Measures investor confidence in Europe's largest economy and signals potential ECB policy direction.

• Canadian Inflation Rate YoY at 13:30 BST - Previous: 1.7% - Critical for Bank of Canada rate decisions and CAD direction as inflation remains below target.

• US Retail Sales MoM at 13:30 BST - Forecast: 0.3% vs Previous: 0.5% - Primary gauge of consumer spending strength that drives two-thirds of US economic activity.

• Japanese Balance of Trade at 00:50 BST (Wednesday) - Forecast: ¥-513.6B vs Previous: ¥-118.4B - Significant deterioration expected in trade balance could pressure the yen and influence BOJ policy stance.

• Ferguson Enterprises Inc. (FERG) at 11:45 GMT [Pre-Market] - Est: $3.01 vs Prev: $2.50 - Major building materials distributor's results will signal construction sector health and North American infrastructure spending trends.

• JTC Plc (JTC) at 07:00 GMT [Pre-Market] - Est: N/A vs Prev: N/A - Leading fund services provider's performance offers insights into alternative investment flows and institutional asset management demand.

• Park24 Co., Ltd. (4666) at 13:00 GMT [Pre-Market] - Est: $0.21 vs Prev: $-0.01 - Japan's largest parking operator results reflect urban mobility recovery and consumer spending patterns in Asia's second-largest economy.

• NEW HOPE CORPORATION LIMITED (NHC) at 13:00 GMT [Pre-Market] - Est: $0.07 vs Prev: $0.24 - Australian coal producer's earnings will indicate commodity demand strength and energy transition impacts on traditional mining operations.

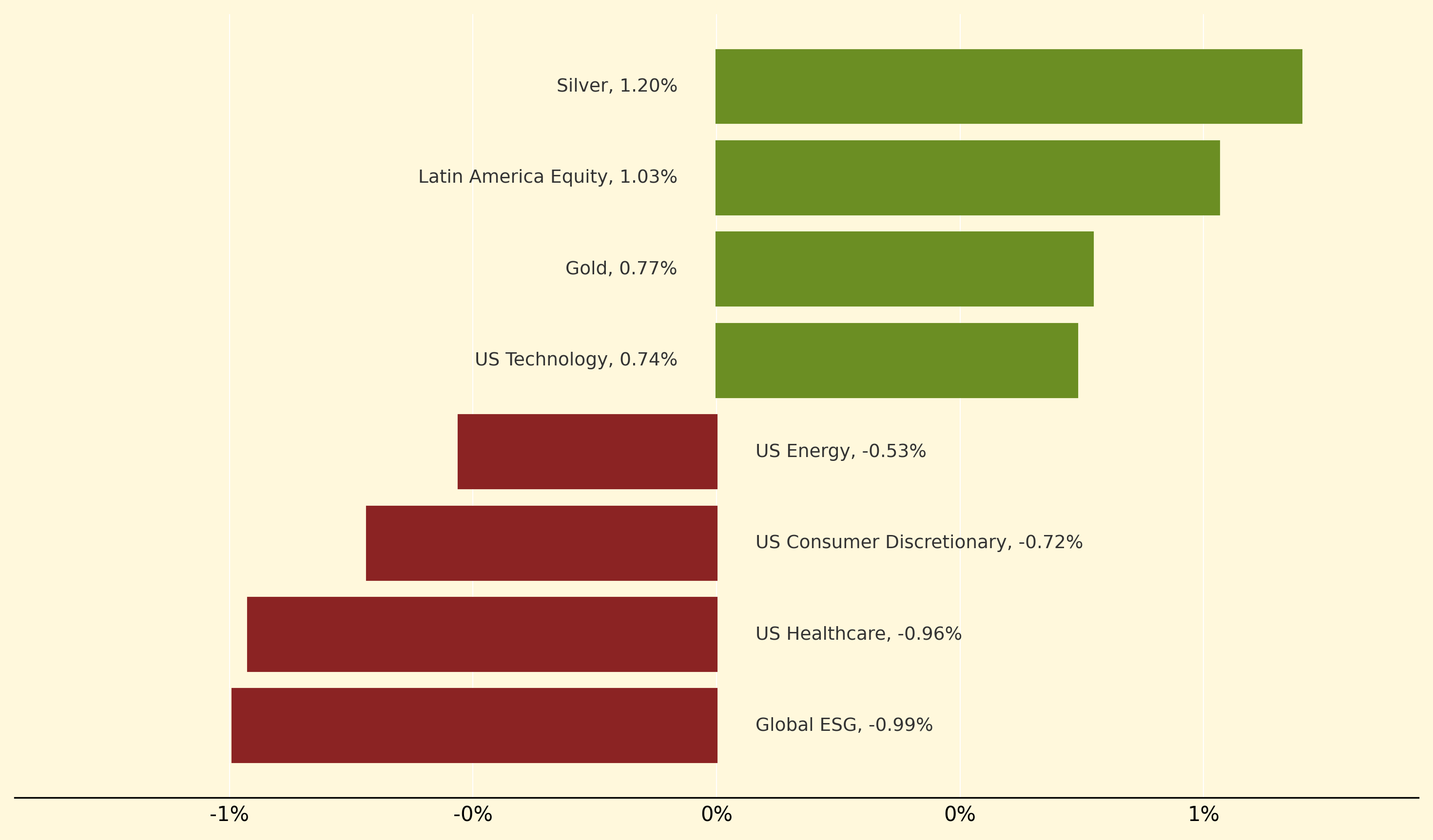

Silver led precious metals higher, climbing 1.2% as dollar weakness ahead of the Fed meeting boosted commodity appeal, whilst Latin America Equity gained 1.03% and Gold advanced 0.77% to fresh records. US Technology and US Large-Cap Growth also posted solid gains of 0.74% and 0.6% respectively, benefiting from the broader risk-on sentiment driving markets to new highs.

Conversely, Global ESG strategies underperformed significantly, dropping 0.99% as investors rotated away from thematic plays towards momentum trades. US Healthcare fell 0.96% and US Consumer Discretionary declined 0.72%, whilst US Energy dropped 0.53% despite geopolitical supply concerns from Ukrainian attacks on Russian facilities, suggesting Fed easing expectations outweighed sector-specific catalysts.

Systemic uncertainty: The risk that disruptions to core financial institutions or market infrastructure could cascade through interconnected systems, potentially triggering widespread economic instability. In this context, political interference with Fed independence creates systemic uncertainty because the central bank's credibility underpins global dollar policy and monetary transmission mechanisms worldwide.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry