Fed Policy Uncertainty Drives Global Repricing as Powell Warns on Valuations | Links: [1], [2], [3], [4]

Federal Reserve Chair Powell delivered his most cautious assessment yet on future rate cuts yesterday, describing current equity valuations as "fairly highly valued" whilst warning there's no "risk-free path" for monetary policy decisions. The comments triggered broad market declines, breaking record-high streaks and strengthening the dollar against sterling and other major currencies as traders recalibrated expectations for December's FOMC meeting. Powell maintained that further cuts remain likely but emphasised the need to balance inflation versus employment risks carefully. The mixed signals created fresh uncertainty as Fed officials offered contrasting views - Chicago Fed President Goolsbee cautioned against "overly frontloading" cuts whilst San Francisco Fed's Daly supported continued easing. This internal divergence comes as markets had grown comfortable with aggressive easing expectations, leaving fund managers reassessing duration positioning and cross-currency strategies.

EU Proposes €130 Billion Ukraine 'Reparations Loan' Using Frozen Russian Assets | Links: [5], [6], [7]

European officials unveiled plans for a potential €130 billion "reparations loan" to Ukraine, utilising frozen Russian sovereign assets worth approximately €200 billion held across Western institutions. The mechanism represents a dramatic escalation in economic warfare, proposing to use interest generated from frozen assets to seize principal amounts directly. European finance ministers frame this as converting Russian assets into "Ukrainian firepower," creating dangerous legal precedent for sovereign asset seizure whilst circumventing traditional lending structures. The scale dwarfs previous aid packages and signals sustained Western commitment to Ukraine's reconstruction and defence capabilities. However, the proposal raises fundamental questions about sovereign immunity and international law that could reshape how nations manage reserves globally, particularly those under potential sanctions risk.

Copper Surges to Year Highs on Major Mine Supply Disruption | Links: [8], [9]

Goldman Sachs slashed copper supply forecasts after Freeport's Indonesian Grasberg mine warned it cannot meet customer contracts, removing 525,000 tons from global production and shifting markets from surplus to deficit. Copper prices jumped to seven-week highs as the world's second-largest copper mine cited infrastructure issues affecting approximately 1.5% of global copper output. The supply shock sent immediate ripple effects across industrial metals markets, with manufacturing sectors facing potential cost pressures whilst commodity traders adjusted positioning amid suddenly tight fundamentals. The disruption highlights critical vulnerability in global supply chains for industrial materials, particularly as electrification and energy transition demands continue rising. Industrial metals portfolios benefited immediately whilst broader commodity markets reassessed supply security across the complex.

US Government Eyes Direct Equity Stake in Lithium Americas | Links: [10], [11]

Lithium Americas surged 90-95% yesterday on reports the Trump administration is considering taking direct equity stakes in critical mineral mining companies, marking a notable shift in US industrial policy. The potential government investment represents a dramatic departure from traditional subsidies or loans, potentially creating state ownership in private mining operations as Washington addresses China's lithium processing dominance. This evolution toward direct state capital deployment for strategic objectives could extend to other critical materials sectors as the US seeks supply chain independence from geopolitical rivals. The equity stake approach signals major philosophical shift from free-market policies toward active industrial strategy, with implications extending far beyond lithium into broader critical minerals supply chains. Treasury Secretary Bessent's background suggests this direct intervention model could become standard practice for strategic sectors under the new administration.

Credit Markets Face Twin Pressures as US Lending Standards Deteriorate | Links: [12], [13], [14], [15]

US credit markets are flashing warning signals as lending standards deteriorate rapidly, with debt investors raising alarms over declining underwriting quality following unexpected corporate failures. DoubleLine Asset Management questioned the reliability of Bureau of Labor Statistics employment data, suggesting economic indicators may be understating labour market weakness at a critical juncture for corporate refinancing. The twin pressures of data integrity and actual lending standard degradation create dangerous feedback loops, particularly given elevated corporate leverage and upcoming maturity walls. Credit spreads remain compressed despite these warning signals, suggesting potential mispricing of default risk across investment-grade and high-yield markets. Shadow banking proliferation adds another layer of complexity as alternative credit vehicles face heightened scrutiny amid concerns about contagion risks spreading beyond traditional banking channels.

| Dow Jones Industrial Average | --▼ -0.53% |

| S&P 500 | --▼ -0.48% |

| Hang Seng Index | --▲ +1.71% |

| FTSE 100 | --▲ +0.29% |

| CAC 40 | --▼ -0.56% |

| DAX 40 | --▲ +0.28% |

| Euro Stoxx 50 | --▼ -0.14% |

| Nasdaq Composite | --▼ -0.70% |

| Nasdaq-100 | --▼ -0.59% |

| Nikkei 225 | --▲ +0.32% |

| S&P/ASX 200 | --▼ -0.92% |

| Shanghai Composite | --▲ +1.29% |

| S&P 500 E-mini | 6698.50+6.25▲ +0.09% |

| Nasdaq-100 | 24752.20+13.00▲ +0.05% |

| FTSE 100 Index | 9280.50-24.00▼ -0.26% |

| EURO STOXX 50 | 5478.00-3.00▼ -0.05% |

| WTI Crude Oil | 64.62-0.37▼ -0.57% |

| Gold (COMEX) | 3765.40-2.70▼ -0.07% |

| Copper (COMEX) | 4.87+0.06▲ +1.26% |

| US 10-Year Treasury | 112.66+0.02▲ +0.01% |

| UK Long Gilt (10Y) | 117.72+0.03▲ +0.03% |

| German Bund (10Y) | 128.20+0.01▲ +0.01% |

| Italian BTP (10Y) | 119.52-0.15▼ -0.13% |

| US Dollar Index | 97.41-0.10▼ -0.10% |

| VIX Volatility | 17.95-0.09▼ -0.51% |

| SONIA 3M Interest Rate | 96.14+0.00▲ +0.01% |

• German GfK Consumer Confidence at 07:00 BST - Forecast: -23.0 vs Previous: -23.6 - Key gauge of Eurozone's largest economy consumer sentiment, affecting EUR strength and ECB policy expectations.

• US GDP Growth Rate QoQ Final at 13:30 BST - Forecast: 3.3% vs Previous: -0.5% - Final revision could confirm robust US economic momentum, influencing Fed policy path and USD strength.

• US Durable Goods Orders MoM at 13:30 BST - Forecast: -0.4% vs Previous: -2.8% - Manufacturing demand indicator that signals business investment trends and industrial sector health.

• US Initial Jobless Claims at 13:30 BST - Forecast: 240,000 vs Previous: 231,000 - Weekly labour market pulse affecting Fed rate expectations and USD sentiment.

• UK CBI Distributive Trades at 11:00 BST - Forecast: -26.0 vs Previous: -32.0 - Retail sector health indicator amid UK consumer spending pressures and BoE policy considerations.

• US Goods Trade Balance Adv at 13:30 BST - Forecast: -$95.2B vs Previous: -$103.6B - Trade deficit trends affecting USD and providing insight into US economic competitiveness.

• H&M Hennes & Mauritz AB Class B (HM_B) at 07:00 BST [Pre-Market] - Est: $0.17 vs Prev: $0.26 - European retail bellwether's results will signal consumer spending trends across fashion retail sector.

• Jabil Inc. (JBL) at 12:45 BST [Pre-Market] - Est: $2.91 vs Prev: $2.55 - Electronics manufacturing giant's guidance will provide insights into global supply chain conditions and tech demand.

• Oracle Corporation Japan (4716) at 13:00 BST [Pre-Market] - Est: $0.81 vs Prev: $0.86 - Regional Oracle performance offers window into enterprise software adoption in Asian markets.

• Washington H. Soul Pattinson and Co. Ltd. (SOL) at 13:00 BST [Pre-Market] - Est: TBD vs Prev: $0.61 - Australia's oldest listed investment company results impact diversified portfolio and mining exposure sentiment.

• Accenture plc (ACN) at 14:30 BST [During-Hours] - Est: $2.97 vs Prev: $3.49 - Mega-cap consulting leader's results will drive sentiment across professional services and digital transformation sectors.

• TD SYNNEX Corporation (SNX) at 14:30 BST [During-Hours] - Est: $3.05 vs Prev: $2.99 - Technology distribution giant's performance indicates health of IT infrastructure spending globally.

• LPP S.A. (LPP) at 15:30 BST [During-Hours] - Est: $54.99 vs Prev: $47.89 - Eastern European fashion retailer's results will influence broader European retail and emerging market consumer sentiment.

• Costco Wholesale Corporation (COST) at 21:15 BST [During-Hours] - Est: $5.80 vs Prev: $4.28 - Mega-cap warehouse club's membership trends and margins will impact broader retail and consumer discretionary sectors.

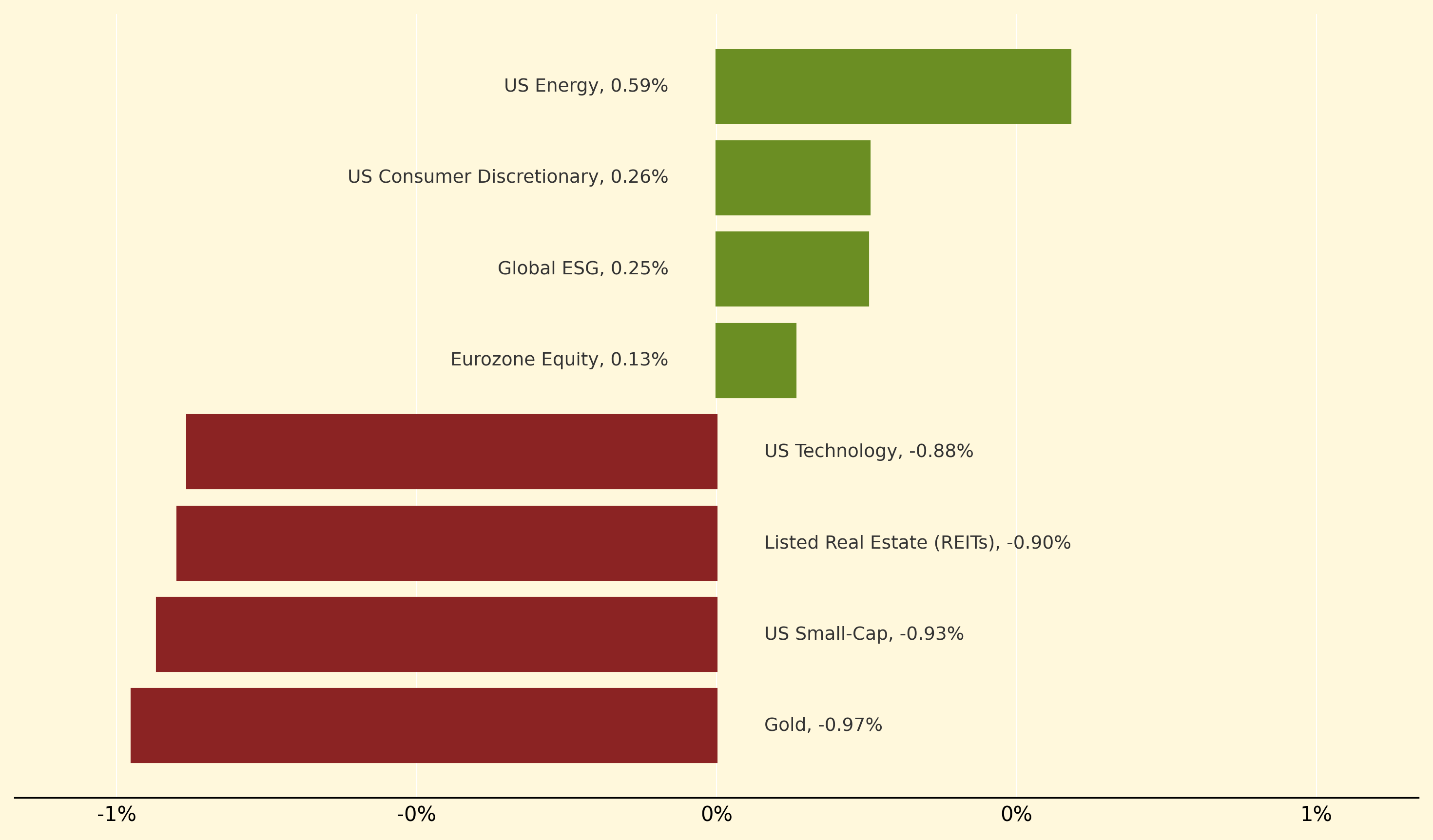

US Energy led yesterday's gains, climbing 0.59% as copper supply disruptions and government backing for critical mineral companies boosted the sector. US Consumer Discretionary also advanced 0.26%, whilst Global ESG strategies gained 0.25% despite broader market headwinds following Powell's cautious Fed commentary.

Conversely, Gold underperformed significantly, dropping 0.97% as the dollar strengthened following Powell's warnings about elevated equity valuations. US Small-Cap and REITs also lagged, falling 0.93% and 0.90% respectively, whilst US Technology declined 0.88% amid the Fed Chair's valuation concerns and broader risk-off sentiment following his hawkish tone on future rate cuts.

Maturity walls: Concentrated periods when large volumes of corporate debt come due for refinancing, creating systemic risk if credit markets tighten or companies cannot roll over their obligations successfully.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry