US Dollar Under Pressure as Government Shutdown Looms and Fed Policy Diverges | Links: [1], [2], [3], [4], [5]

The greenback faces a perfect storm of political uncertainty and monetary confusion, down 9.5% this year as multiple pressures converge. Government shutdown risks threaten to delay crucial September payrolls data just as the Fed prepares for its October meeting, whilst contradictory economic signals complicate policy decisions. Consumer spending beat estimates in August, demonstrating economic resilience, but core PCE inflation held stubbornly at 2.9% as expected—exactly where the Fed finds it problematic. Adding to the uncertainty, Fed Governor Miran's controversial call for 200 basis points of rate cuts has sparked internal tensions and technical corrections to his immigration-inflation analysis. PGIM executives warn the currency could weaken further if Trump successfully pressures the central bank toward excessive dovishness, creating a monetary policy credibility crisis that markets are already pricing into currency positioning.

Gold Smashes Through $3,800 as Safe-Haven Demand Surges | Links: [6], [7], [8]

Gold has blasted past $3,800 per ounce for the first time, driven by the toxic combination of dollar weakness and mounting geopolitical uncertainty. The precious metal's surge reflects a broader flight to safety as investors seek portfolio insurance against currency debasement and political chaos. The breakout above this psychological milestone signals serious risk-off sentiment across markets, with rate cut expectations reducing gold's opportunity cost whilst dollar weakness makes it more attractive to international buyers. This rally represents more than just technical momentum—it's a barometer of confidence in traditional monetary systems as central banks struggle with conflicting mandates and political pressure. The metal's appeal has intensified as real yields turn negative and investors question whether conventional assets can provide adequate protection in an era of unprecedented monetary experimentation.

US Market Valuation Concerns Mount as Buffett Indicator Tops 200% | Links: [9], [10]

The Buffett Indicator has breached 200% for the first time—a level Warren Buffett once described as "playing with fire"—representing the most extreme stock market valuation relative to GDP on record. This dangerous milestone coincides with growing debate over whether artificial market resilience is actually preventing necessary economic adjustments, creating potentially harmful imbalances. The wealth effects from elevated stock prices may be supporting consumer spending and keeping recession at bay, but economists warn this creates vulnerability to sharp reversals that could amplify economic downturns. Market resilience, typically viewed as positive, may paradoxically prove harmful by delaying natural corrections and allowing dangerous bubbles to inflate further. The combination of record valuations and monetary policy artificiality indicates markets are operating in uncharted territory where traditional risk metrics may underestimate the potential for severe corrections.

UK Faces Twin Pressures as Pound Slides and Fiscal Concerns Mount | Links: [11], [12], [13], [14]

Sterling suffered its biggest weekly decline since July as fiscal sustainability fears collide with deteriorating economic fundamentals ahead of November's crucial budget. The pound's weakness reflects growing concerns about Chancellor Reeves' ability to balance ambitious spending plans with market credibility, whilst falling job postings and downbeat business sentiment signal labour market cooling. Bank of England MPC member Dhingra has called for faster interest rate cuts, adding to policy divergence within the committee just as the central bank needs to project unity. Despite the BoE's confidence that gilt markets withstood recent global turbulence, rising yields and pre-budget uncertainty are testing investor appetite for UK assets. The combination of weak economic data, fiscal concerns, and monetary policy confusion creates a challenging backdrop for sterling as markets question whether Britain can maintain its delicate balance between growth ambitions and fiscal discipline.

Central Bank Policy Divergence Accelerates as Global Tensions Rise | Links: [15], [16], [17], [18]

The week's central bank developments highlight accelerating policy divergence as major economies grapple with distinct domestic challenges. The Bank of Japan delivered the biggest surprise, with two dissenting votes for rate hikes significantly raising October tightening probability and lowering the bar for policy normalisation. This contrasts sharply with eurozone dynamics, where inflation hit a five-month high but the ECB remains anchored to its cautious approach whilst advancing digital euro experiments for 2026. Meanwhile, geopolitical complexity is adding another layer of uncertainty—OPEC+ plans another oil output increase in November despite Ukrainian attacks on Russian energy infrastructure threatening supply stability. The combination of monetary policy uncertainty and escalating geopolitical tensions creates a treacherous environment for global asset allocation as markets navigate conflicting signals about growth, inflation, and risk. Central bankers are increasingly operating in isolation rather than coordination, suggesting volatility will remain elevated as policy paths diverge further.

| Dow Jones Industrial Average | --▲ +0.32% |

| S&P 500 | --▲ +0.43% |

| Hang Seng Index | --▼ -0.55% |

| FTSE 100 | --▲ +0.77% |

| CAC 40 | --▲ +0.62% |

| DAX 40 | --▲ +0.59% |

| Euro Stoxx 50 | --▲ +0.93% |

| Nasdaq Composite | --▲ +0.36% |

| Nasdaq-100 | --▲ +0.38% |

| Nikkei 225 | --▼ -0.61% |

| S&P/ASX 200 | --▲ +0.17% |

| Shanghai Composite | --▼ -0.31% |

| S&P 500 E-mini | 6718.75+22.25▲ +0.33% |

| Nasdaq-100 | 24832.00+105.25▲ +0.43% |

| FTSE 100 Index | 9360.00+32.00▲ +0.34% |

| EURO STOXX 50 | 5535.00+25.00▲ +0.45% |

| WTI Crude Oil | 65.30-0.42▼ -0.64% |

| Gold (COMEX) | 3831.60+22.60▲ +0.59% |

| Copper (COMEX) | 4.81+0.04▲ +0.76% |

| US 10-Year Treasury | 112.44+0.17▲ +0.15% |

| UK Long Gilt (10Y) | 117.70+0.05▲ +0.04% |

| German Bund (10Y) | 128.37+0.11▲ +0.09% |

| Italian BTP (10Y) | 119.46+0.24▲ +0.20% |

| US Dollar Index | 97.60-0.22▼ -0.23% |

| VIX Volatility | 17.40-0.10▼ -0.53% |

| SONIA 3M Interest Rate | 96.12+0.00▲ +0.00% |

• Chinese NBS Manufacturing PMI on Tuesday at 02:30 BST - Forecast: 49.6 vs Previous: 49.4 - Key gauge of China's factory activity, critical for global growth outlook and commodity demand.

• Chinese RatingDog Manufacturing PMI on Tuesday at 02:45 BST - Forecast: 50.3 vs Previous: 50.5 - Alternative PMI reading that often moves markets, particularly important for assessing China's economic momentum.

• Australian RBA Interest Rate Decision on Tuesday at 05:30 BST - Forecast: 3.6% vs Previous: 3.6% - RBA expected to hold rates steady, but commentary will be watched for policy pivot signals affecting AUD.

• French Inflation Rate YoY on Tuesday at 07:45 BST - Forecast: 1.3% vs Previous: 0.9% - Sharp uptick expected in French inflation, key input for ECB policy decisions and eurozone rate expectations.

• German Inflation Rate YoY on Tuesday at 13:00 BST - Forecast: 2.3% vs Previous: 2.2% - Germany's inflation trend crucial for ECB policy stance and euro direction.

• US JOLTs Job Openings on Tuesday at 15:00 BST - Forecast: 7.1M vs Previous: 7.181M - Fed closely watches job openings for labour market tightness, influencing rate cut timing.

• Japanese Tankan Large Manufacturers Index on Wednesday at 00:50 BST - Forecast: 15.0 vs Previous: 13.0 - Bank of Japan's key business sentiment survey, critical for yen and Japanese equity markets.

• EU Inflation Rate YoY Flash on Wednesday at 10:00 BST - Forecast: 2.3% vs Previous: 2.0% - Eurozone inflation acceleration could delay ECB easing, supporting euro strength.

• US ISM Manufacturing PMI on Wednesday at 15:00 BST - Forecast: 49.2 vs Previous: 48.7 - Manufacturing sector health indicator, with readings below 50 signalling contraction affecting industrial stocks.

• Australian Balance of Trade on Thursday at 02:30 BST - Forecast: A$6.5B vs Previous: A$7.31B - Trade surplus trends impact AUD and reflect commodity export strength.

• US Non Farm Payrolls on Friday at 13:30 BST - Forecast: 39K vs Previous: 22K - Critical employment data that will heavily influence Fed rate cut expectations and USD direction.

• US ISM Services PMI on Friday at 15:00 BST - Forecast: 52.0 vs Previous: 52.0 - Services sector dominates US economy, key for assessing domestic demand strength and Fed policy path.

• Tesco PLC (TSCO) on Thursday at 07:00 BST Pre-Market - $38.3B - UK's largest retailer and FTSE 100 heavyweight will provide crucial insights into consumer spending patterns and inflation impact on grocery sector.

• Zegona Communications Plc (ZEG) on Monday at 13:00 BST Pre-Market - $12.5B - European telecom investment company's results will signal sector consolidation trends and regulatory developments across key markets.

• Nitori Holdings Co. Ltd. (9843) on Thursday at 13:00 BST Pre-Market - $10.7B - Japan's leading furniture retailer will indicate Asian consumer discretionary spending and supply chain recovery post-pandemic disruptions.

• VinFast Auto Ltd. (VFS) on Thursday at 13:00 BST Pre-Market - $7.4B - Vietnamese EV manufacturer's earnings will reflect emerging market EV adoption and competition with established automakers in global markets.

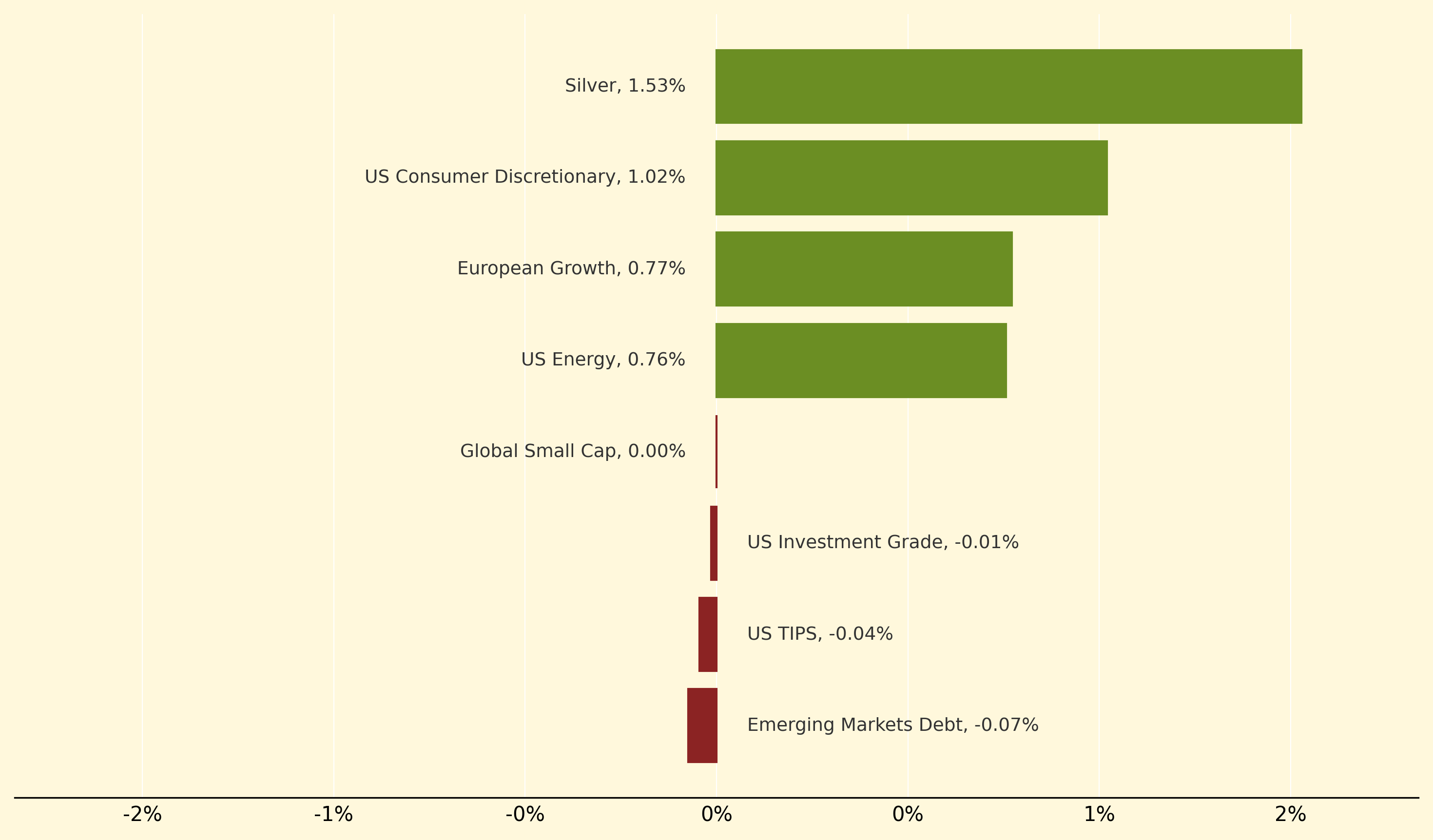

Silver led the commodities surge, climbing 1.53% as greenback weakness and safe-haven demand boosted precious metals appeal alongside gold's record-breaking rally past $3,800. US Consumer Discretionary advanced 1.02% despite mounting valuation concerns, with solid August consumer spending data demonstrating economic resilience even as the Buffett Indicator breached dangerous 200% territory.

Fixed income strategies struggled amid rate cut uncertainty and policy confusion, with Emerging Markets Debt declining 0.07% as central bank policy divergence accelerated globally. US TIPS fell 0.04% as real yields remained pressured by conflicting Fed signals, whilst traditional bond categories like US Investment Grade and UK Fixed Income posted minimal losses as markets grappled with government shutdown risks and fiscal sustainability concerns.

Policy divergence: The simultaneous pursuit of different monetary policy directions by major central banks, creating currency volatility and complicating global investment strategies as economies face distinct domestic challenges requiring conflicting approaches.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry