Global Equity Rally Powers Through Political Noise as Tech Momentum Accelerates | Links: [1], [2], [3]

World markets extended their six-day winning streak to fresh records yesterday, with the S&P 500 achieving all-time highs despite the US government shutdown grinding into its third day. The index now trades at 23.1x forward earnings as institutional appetite for risk assets remains unshaken, buoyed by Fed rate cut expectations reaching 95% probability for December. European stocks achieved record closes with the STOXX 600 benefiting from synchronised tech sector gains, while Asia-Pacific markets joined the global rally on artificial intelligence optimism. Technology continues to lead the charge with notable developments including Hitachi surging 9% on its OpenAI partnership and Intel climbing 50% over the month on AI infrastructure hopes.

Fed Policy Divergence Reshapes Global Fixed Income as Central Banks Signal Different Paths | Links: [4], [5], [6]

Central bank communication revealed significant policy divergence signals that are transforming fixed income markets across major economies. Fed Vice Chair Logan warned against cutting rates too aggressively, citing tariff-driven inflation concerns, even as markets maintain overwhelming confidence in December easing. Across the Pacific, BOJ Governor Ueda deliberately avoided clear rate hike signals despite positive Tankan business sentiment data, though markets still price over 60% probability of October tightening that could strengthen the yen substantially. Meanwhile, the ECB's Kazaks provided forward guidance suggesting rates could stabilise at 2% absent external shocks, while the US government shutdown complicates the Fed's October meeting by limiting crucial economic data availability. This divergence creates substantial opportunities across currencies and sovereigns.

US Labour Market Stagnation Deepens Despite Political Shutdown Noise | Links: [7], [8]

Beneath the political theatre of Washington's shutdown lies a more troubling economic reality: US employment data reveals planned hiring intentions at 16-year lows despite falling layoffs. Job openings remain moderate while hiring activity shows persistent weakness, painting a picture of labour market stagnation that contrasts sharply with equity market euphoria. The government shutdown compounds this uncertainty by limiting official data availability, forcing economists to rely on alternative sources showing unemployment steady at 4.3% but with underlying structural weakness persisting. This deterioration provides additional justification for Fed dovishness while highlighting the growing disconnect between financial markets trading at record valuations and fundamental economic conditions on the ground.

Berkshire Hathaway Makes $9.7 Billion Industrial Bet as Buffett Signals Confidence | Links: [9]

Warren Buffett deployed $9.7 billion of Berkshire Hathaway capital to acquire Occidental's chemical division, representing one of the year's most significant industrial transactions and a powerful vote of confidence in US manufacturing assets. The deal demonstrates the Oracle of Omaha's continued appetite for traditional industrial consolidation opportunities while broader markets chase technology momentum, potentially indicating where he sees genuine value amid stretched market conditions. This major capital deployment into chemicals comes as the sector faces consolidation pressures and provides insight into value investing strategy during a period of concentrated tech leadership. The acquisition also demonstrates Berkshire's substantial dry powder availability and willingness to act decisively when attractive opportunities emerge in overlooked sectors.

Gold's Historic Run and European Strategic Pivot Signal Fundamental Shifts in Global Finance | Links: [10], [11], [12]

Gold advanced to a seventh consecutive weekly gain, approaching $4,000 with 47% year-to-date returns as haven demand intensifies amid government shutdown uncertainty and Fed easing expectations. This remarkable rally coincides with Europe's strategic push for monetary autonomy, as ECB policymaker Villeroy urgently called for bolstering the euro's global role by 2028 through expanded ties with countries affected by US tariffs, including India, Switzerland, and Indonesia. The central bank also selected an AI startup for €237 million to prevent digital euro fraud, marking concrete progress toward the 2029 launch. These parallel developments reflect growing institutional concerns about dollar dominance and potential structural shifts in the global monetary system, as traditional safe-haven flows combine with deliberate efforts to reduce dependence on US financial infrastructure.

| Dow Jones Industrial Average | --▲ +0.13% |

| S&P 500 | --▼ -0.24% |

| Hang Seng Index | --▲ +1.37% |

| FTSE 100 | --▼ -0.20% |

| CAC 40 | --▲ +0.39% |

| DAX 40 | --▲ +0.53% |

| Euro Stoxx 50 | --▲ +0.51% |

| Nasdaq Composite | --▼ -0.18% |

| Nasdaq-100 | --▼ -0.16% |

| Nikkei 225 | --▲ +0.45% |

| S&P/ASX 200 | --▲ +1.13% |

| S&P 500 E-mini | 6781.75+15.00▲ +0.22% |

| Nasdaq-100 | 25179.80+69.75▲ +0.28% |

| FTSE 100 Index | 9493.50+14.50▲ +0.15% |

| EURO STOXX 50 | 5677.00+9.00▲ +0.16% |

| WTI Crude Oil | 60.93+0.45▲ +0.74% |

| Gold (COMEX) | 3878.80+10.70▲ +0.28% |

| Copper (COMEX) | 4.96+0.01▲ +0.12% |

| US 10-Year Treasury | 112.86-0.06▼ -0.06% |

| UK Long Gilt (10Y) | 117.85+0.00▲ +0.00% |

| German Bund (10Y) | 128.66+0.01▲ +0.01% |

| Italian BTP (10Y) | 119.90-0.03▼ -0.03% |

| US Dollar Index | 97.61+0.02▲ +0.02% |

| VIX Volatility | 17.75-0.09▼ -0.52% |

| SONIA 3M Interest Rate | 96.12-0.01▼ -0.01% |

• US Unemployment Rate at 13:30 BST - Forecast: 4.3% vs Previous: 4.3% - Key labour market indicator that influences Fed policy decisions and USD strength.

• US Non Farm Payrolls at 13:30 BST - Forecast: 39.0K vs Previous: 22.0K - Critical employment data that drives Fed rate expectations and market volatility across equities and bonds.

• US ISM Services PMI at 15:00 BST - Forecast: 52.0 vs Previous: 52.0 - Measures the dominant services sector's health, impacting USD and broader market sentiment on economic growth.

• EU ECB President Lagarde Speech at 10:40 BST - Central bank communication that could indicate future monetary policy direction and impact EUR positioning.

• GB BoE Gov Bailey Speech at 14:20 BST - BoE policy insights that may influence GBP and UK gilt yields amid ongoing inflation concerns.

• French Industrial Production MoM at 07:45 BST - Forecast: 0.3% vs Previous: -1.1% - Recovery indication for eurozone manufacturing could support EUR and European equity markets.

• Zegona Communications Plc (ZEG) at 13:00 BST [Pre-Market] - Est: N/A vs Prev: N/A - Telecom consolidation play could signal broader European telecoms M&A activity and sector rotation trends.

• Yaskawa Electric Corporation (6506) at 13:00 BST [Pre-Market] - Est: $0.19 vs Prev: $0.19 - Industrial automation leader's results may indicate global manufacturing demand and robotics sector health amid economic uncertainty.

• Kernel Holding S.A. (KER) at 15:30 BST [During-Hours] - Est: N/A vs Prev: N/A - Ukrainian agribusiness giant's performance reflects geopolitical impact on global food supply chains and commodity markets.

• Top Glove Corporation Bhd. (TOPGLOV) at 13:00 BST [Pre-Market] - Est: $0.00 vs Prev: $0.00 - World's largest glove manufacturer results indicate post-pandemic healthcare supply normalization and emerging market resilience.

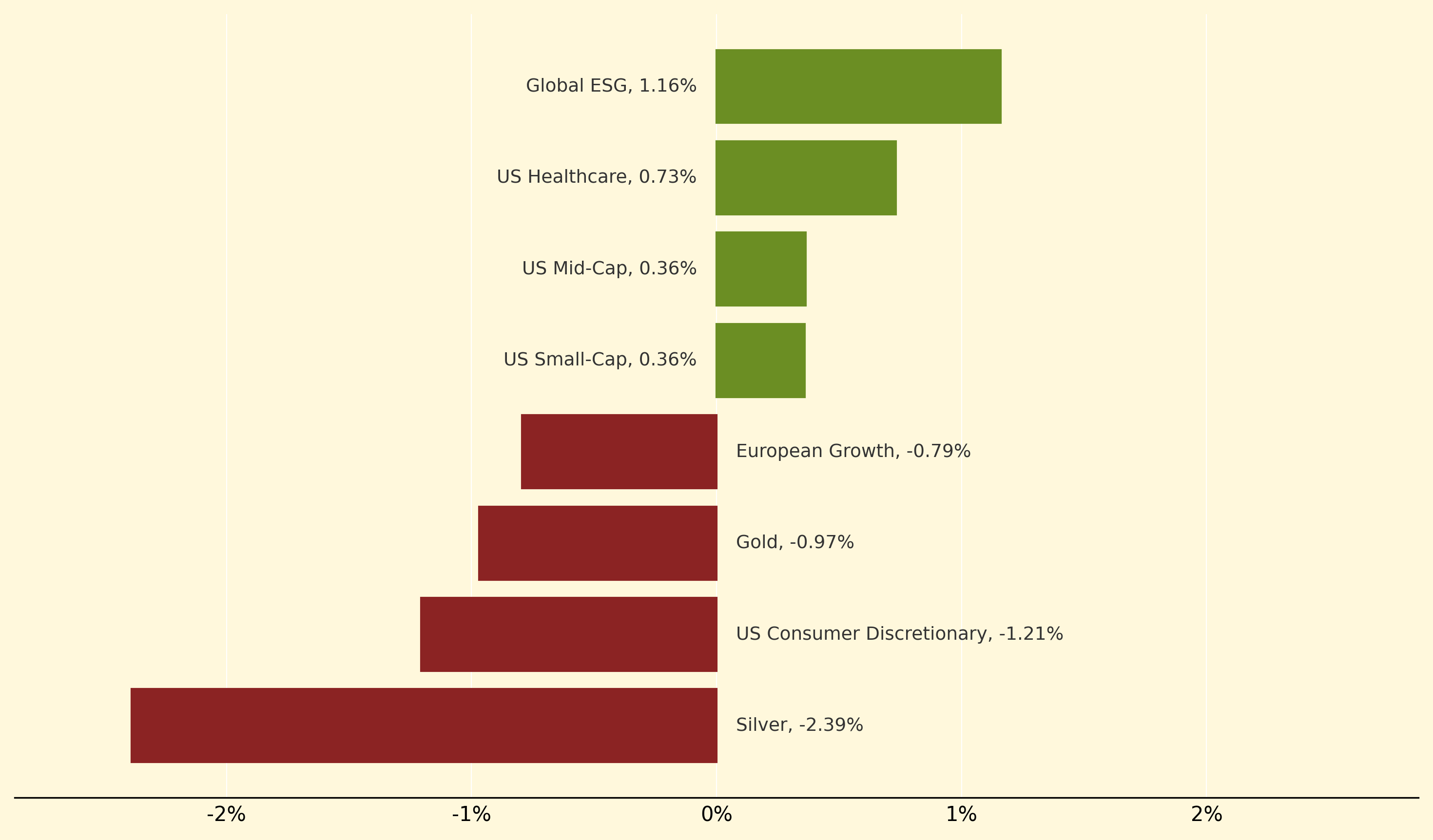

Global ESG strategies topped the market with a 1.16% gain, benefiting from renewed institutional interest as UBS wealth executives highlighted new client demand driving ESG revival. US Healthcare also performed strongly, advancing 0.73% amid the broader tech-supported rally, while mid-cap and small-cap US strategies posted modest 0.36% gains as domestic equity momentum remained concentrated in larger names.

Precious metals faced significant pressure, with Silver declining 2.39% and Gold dropping 0.97% despite its approach toward a seventh consecutive weekly gain on rate-cut expectations. US Consumer Discretionary fell 1.21% as labour market stagnation concerns weighed on spending outlooks, while US Energy declined 0.79% alongside oil's steep weekly losses driven by oversupply concerns ahead of the OPEC+ meeting.

Forward guidance: Central bank communication about future monetary policy intentions designed to influence market expectations and economic behaviour without immediate rate changes, providing markets with policy trajectory signals that shape investment decisions and economic planning.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry