Precious Metals Rally to Record Highs Amid Perfect Storm of Safe-Haven Demand | Links: [1], [2], [3]

Gold has reached unprecedented heights above $4,100 per ounce, whilst silver shattered all-time records beyond $52.50, as multiple risk factors converge to drive extraordinary demand for hard assets. The yellow metal's 58% year-to-date advance reflects Federal Reserve rate cut expectations, intensifying US-China trade tensions, and supply disruptions in London precious metals markets. Silver's breakthrough stems from structural supply constraints and portfolio spillover effects from gold's relentless ascent. London market participants report supply bottlenecks creating volatility levels not witnessed in decades. This metals surge represents the clearest market signal yet of underlying stress fracturing the global financial system.

US-China Trade War Escalates with Port Fees and Rare Earth Controls Despite Diplomatic Overtures | Links: [4], [5], [6], [7]

Bilateral trade infrastructure continues fragmenting despite Trump's weekend diplomatic signals, with both nations implementing reciprocal port fees whilst China deploys its rare earth advantage through a sharp 21% export decline in September. Trump's initial tariff threats exceeding 100% created market upheaval before he adopted a more conciliatory tone and suggested meeting Xi Jinping in South Korea, delivering Wall Street's strongest session since May with the S&P 500 advancing 2.21%. However, the underlying commercial architecture keeps deteriorating, with China controlling 90% of processed rare earth markets whilst restricting supplies essential to Western technology, defence, and renewable energy sectors. The Netherlands' unprecedented seizure of Chinese-owned semiconductor firm Nexperia reflects broader Western restrictions on Chinese technology investments. Beyond diplomatic gestures, the new port fees threaten shipping costs and supply chain stability, whilst rare earth controls expose genuine strategic vulnerabilities for Western industry.

Central Banks Issue Stark Warnings on Debt Sustainability and Market Crash Risk | Links: [8], [9], [10], [11]

Global financial stability confronts mounting threats as central bankers abandon diplomatic language for unusually direct warnings about systemic risk. Bank of England Governor Andrew Bailey cautioned that equity markets face crash potential if debt levels spiral uncontrollably, whilst the G20 Financial Stability Board highlighted market crash risks from elevated asset valuations and sovereign debt levels reaching precarious territory. BOE policymaker Megan Greene advocated maintaining rates into 2026 due to persistent price pressures, indicating extended restrictive monetary policy across developed economies. The Economist's comprehensive analysis reveals fiscal crises looming across wealthy nations, with public debt projected to exceed 100% of GDP by 2029 in many developed economies. Fed officials remain divided, with some favouring two additional rate cuts in 2025 whilst looking through tariff impacts, but the combination of high debt levels, elevated asset valuations, and political constraints on fiscal reform creates a dangerous mixture that has alarmed even typically measured central bankers.

JPMorgan Leads Corporate America's $1.5 Trillion 'America First' Investment Push | Links: [12], [13]

JPMorgan Chase has announced a comprehensive $1.5 trillion commitment to strengthen US strategic industries over the next decade, including up to $10 billion specifically designated for national security investments across defence, energy, manufacturing, and technology sectors. This unprecedented corporate pledge aligns with the Trump administration's 'America First' agenda and indicates a broader corporate pivot toward domestic supply chain resilience and critical infrastructure investment. The initiative coincides with the bank's parallel announcement to double its Asia assets to $600 billion by 2030, creating a dual strategy balancing domestic priorities with international expansion amid heightened geopolitical tensions. JPMorgan's commitment represents one of the largest corporate pledges supporting US economic resilience and supply chain independence, potentially reshaping capital allocation across strategically important sectors. The timing suggests corporate America is preparing for a more fragmented, security-focused economic landscape whilst maintaining global reach.

Hedge Funds Shift to Global Industrials While Dumping US Equities | Links: [14]

Institutional capital is repositioning significantly, as hedge funds have turned net short on US equities for the first time in seven weeks whilst aggressively rotating into global industrial sectors, particularly in Europe and Asia. This tactical positioning change by sophisticated investors provides crucial insight into flows that may drive broader market trends, representing a notable momentum shift away from crowded US positions toward undervalued global industrial opportunities. The rotation reflects growing concerns about stretched US market valuations and increased optimism about global industrial demand, particularly in regions benefiting from supply chain diversification away from China. Hedge funds are positioning for geographic and sector performance divergence that may reshape institutional allocation decisions across London trading desks. This shift suggests the era of US equity exceptionalism may be ending, with sophisticated investors already positioning for a world where industrial capacity and geographic diversification trump growth at any price.

| S&P 500 | 6654.72+32.19▲ +0.49% |

| FTSE 100 | 9442.90+15.40▲ +0.16% |

| CAC 40 | 7934.26-25.01▼ -0.31% |

| DAX 40 | 24387.90+15.00▲ +0.06% |

| Dow Jones | 46067.60+369.10▲ +0.81% |

| Euro Stoxx 50 | 5568.19+27.65▲ +0.50% |

| Hang Seng | 25889.50+255.50▲ +1.00% |

| Nasdaq 100 | 24750.20+124.50▲ +0.51% |

| Nasdaq Comp | 22694.60+115.90▲ +0.51% |

| S&P/ASX 200 | 8882.80-75.50▼ -0.84% |

| Shanghai Comp | 3889.50+89.40▲ +2.35% |

| S&P 500 E-mini | 6672.00-22.75▼ -0.34% |

| Nasdaq 100 | 24810.20-112.00▼ -0.45% |

| FTSE 100 | 9463.00-20.00▼ -0.21% |

| Euro Stoxx 50 | 5564.00-10.00▼ -0.18% |

| WTI Crude | 59.48-0.01▼ -0.02% |

| Gold | 4189.60+56.60▲ +1.37% |

| Copper | 5.11-0.04▼ -0.74% |

| US 10Y Treasury | 113.27+0.11▲ +0.10% |

| UK 10Y Gilt | 118.42+0.07▲ +0.06% |

| German 10Y Bund | 129.52+0.12▲ +0.09% |

| Italian 10Y BTP | 120.73+0.12▲ +0.10% |

| US Dollar Index | 98.89-0.12▼ -0.12% |

| VIX Volatility | 19.50+0.47▲ +2.50% |

| SONIA 3M | 96.13+0.00▲ +0.01% |

• UK Unemployment Rate at 07:00 BST - Forecast: 4.7% vs Previous: 4.7% - Key gauge of UK labour market health that influences BoE policy decisions and GBP sentiment.

• German ZEW Economic Sentiment Index at 10:00 BST - Forecast: 39.5 vs Previous: 37.3 - Leading indicator of German economic confidence that impacts EUR strength and broader eurozone outlook.

• US Fed Chair Powell Speech at 17:20 BST - Market-moving commentary on monetary policy direction and economic outlook from the world's most influential central banker.

• UK Average Earnings incl. Bonus (3Mo/Yr) at 07:00 BST - Forecast: 4.7% vs Previous: 4.7% - Critical inflation driver that shapes BoE rate expectations and wage-price spiral concerns.

• China New Yuan Loans at 10:00 BST - Forecast: ¥1472.0B vs Previous: ¥590.0B - Key measure of Chinese credit expansion affecting global growth expectations and commodity demand.

• EU ZEW Economic Sentiment Index at 10:00 BST - Forecast: 30.2 vs Previous: 26.1 - Broad gauge of eurozone economic confidence that influences ECB policy expectations and EUR direction.

No major earnings events scheduled for today.

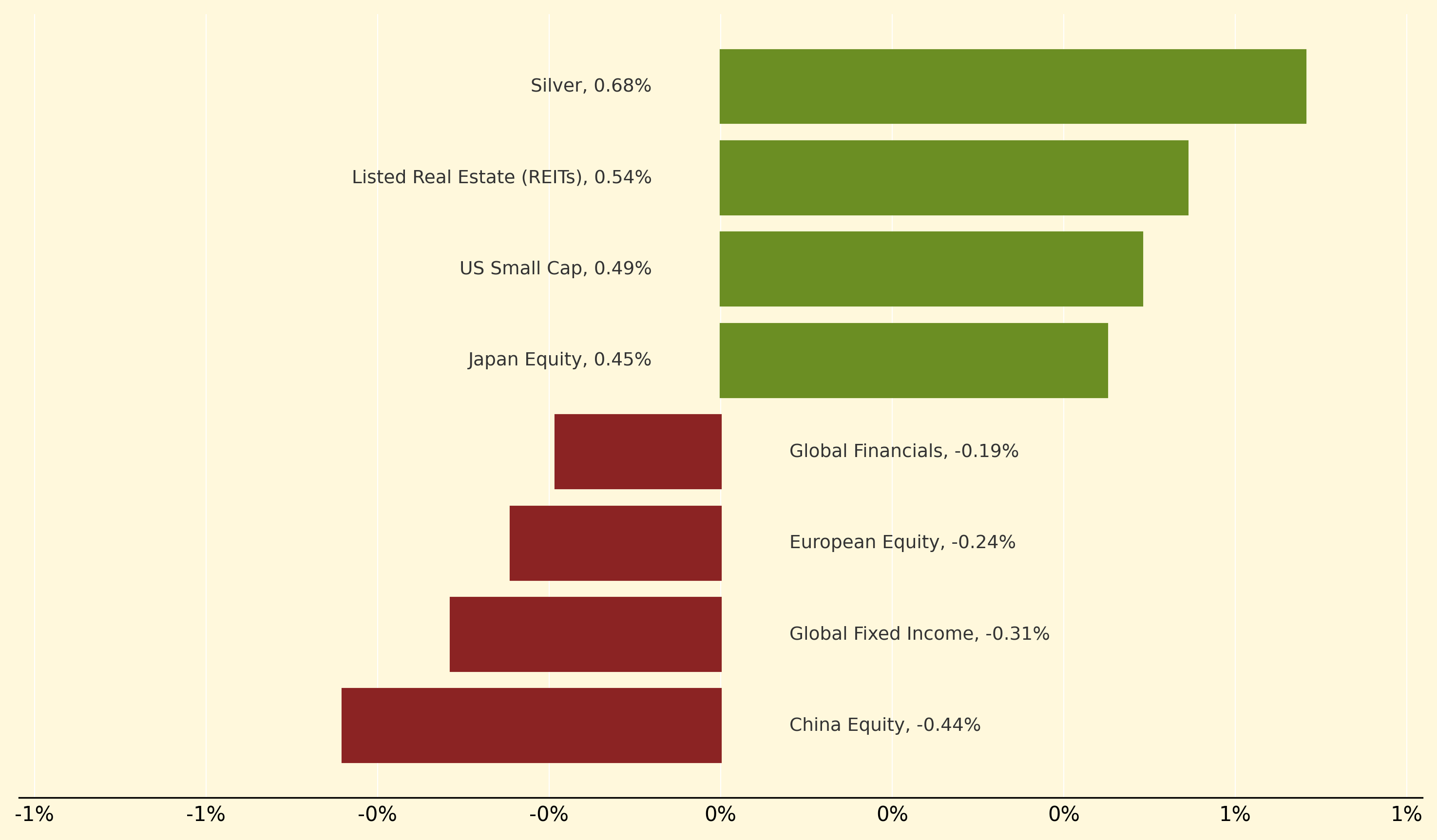

Silver's 0.68% surge led precious metals higher amid the historic rally above $52.50, driven by supply constraints in London markets and safe-haven flows from gold's breakthrough above $4,100. REITs advanced 0.54% alongside US Small Cap's 0.49% gain, as domestic-focused strategies benefited from JPMorgan's $1.5 trillion "America First" investment commitment and reduced trade war concerns following Trump's diplomatic overtures.

China Equity underperformed with a -0.44% decline as intensifying US-China tensions and rare earth export restrictions offset any diplomatic optimism. Global Fixed Income dropped -0.31% following central bank warnings about debt sustainability and potential market crashes, whilst European Equity's -0.24% fall reflected continued concerns over fiscal crises across developed economies despite the temporary trade war reprieve.

Safe-haven spillover: A market phenomenon where flight-to-quality investment flows from one defensive asset cascade into related assets during periods of financial stress or uncertainty, amplifying price movements across the entire safe-haven complex and creating broader risk-off sentiment.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry