Risk-On Versus Safe-Haven Split Defines Markets as Trade Wars Intensify | Links: [1], [2], [3]

Markets delivered contrasting signals yesterday as robust US bank earnings lifted the S&P 500 whilst escalating trade tensions propelled gold beyond previous record highs. Earnings for Morgan Stanley and Bank of America both exceeded expectations, with semiconductor stocks rallying on renewed AI optimism, yet gold surged above prior peaks amid concerns over China's threatened rare earth export controls. This asset class divergence between risk-on equities and defensive precious metals captures the central tension facing investors. Asian markets followed Wall Street's lead, with South Korea's Kospi hitting records on trade deal hopes, whilst currency markets saw dollar weakness as traders positioned for potential Fed easing.

US Escalates China Trade War with Rare Earth Sanctions Threat | Links: [4], [5], [6]

The US-China trade conflict reached a critical inflection point as Beijing imposed export controls on rare earth materials essential for technology and defence industries, prompting threats of 100% retaliatory tariffs from Washington. Treasury Secretary Bessent warned the world will "decouple" from China if the controls are implemented, whilst Trump declared an active trade war and claimed Modi assured him India will halt Russian oil purchases. China's rare earth dominance—controlling 60% of global production and 90% of processing—gives Beijing significant leverage over sectors from electric vehicles to renewable energy infrastructure. Fed Governor Miran directly linked these tensions to monetary policy, suggesting trade uncertainty justifies accelerated rate cuts. The escalation threatens to fragment global supply chains and force costly industrial reorganisation across multiple sectors.

LVMH Sparks $80 Billion Luxury Rally on China Recovery Signs | Links: [7], [8]

LVMH surged 12.2% to its largest daily jump in 20 years after reporting first growth this year, triggering an $80 billion luxury sector rally across Europe. The recovery was driven by improved Chinese consumer demand, with the broader European luxury index benefiting from renewed optimism about high-end consumption patterns in Asia. This dramatic reversal contrasts sharply with months of weakness in European luxury stocks amid concerns about Chinese economic slowdown. The timing proves particularly significant as luxury companies had been among the most exposed to China trade risks, making this recovery signal especially meaningful for global growth expectations. European markets broadly benefited from the luxury surge, with the sector's outsize weighting in major indices amplifying the positive impact across regional equity performance.

Fed Policy Pivot Accelerates as Global Debt Warnings Mount | Links: [9], [10], [11]

Federal Reserve policy recalibration gained momentum as Chair Powell signalled further rate cuts whilst Governor Miran directly linked trade tensions to the need for more aggressive easing. Markets now price increased probability of a half-point cut by year-end, with Fed officials acknowledging that US-China trade uncertainty creates additional downside risks to growth. The policy shift occurs against a backdrop of mounting global debt concerns, with the IMF warning that public debt will exceed 100% of global GDP by 2030—the highest level since World War II. Treasury Secretary Bessent confirmed he will present Fed chair candidates to Trump in December, adding leadership uncertainty to an already complex policy environment. This divergence in central bank positioning—Fed easing, ECB pausing, BOJ gradually tightening—creates complex cross-currency dynamics as coordinated global monetary easing may be required.

AI Investment Boom Faces Reality Check as Infrastructure Demands Surge | Links: [12], [13], [14]

The artificial intelligence investment wave reached new heights with a $40 billion data centre infrastructure deal involving BlackRock, Microsoft, Nvidia, and Singapore's Temasek, whilst TSMC prepared to report record quarterly profits driven by AI chip demand. However, warnings are mounting about sustainability and valuation risks across the sector. A comprehensive analysis identified multiple threats to the "AI gravy train" that now represents nearly 50% of S&P 500 market capitalisation, including capital expenditure spending concerns, return-on-investment questions, and infrastructure bottlenecks. Former IMF chief economist Gita Gopinath warned of potential $35 trillion in wealth destruction from dangerous dependence on US technology stocks. Major asset managers like BlackRock and Fidelity are already scaling back risky credit exposure following the recent rally, suggesting institutional caution emerges even as infrastructure investments accelerate.

| S&P 500 | 6671.06-17.21▼ -0.26% |

| FTSE 100 | 9424.80-28.00▼ -0.30% |

| CAC 40 | 8077.00+47.03▲ +0.59% |

| DAX 40 | 24181.40-82.30▼ -0.34% |

| Dow Jones | 46253.30-121.90▼ -0.26% |

| Euro Stoxx 50 | 5605.03+38.06▲ +0.68% |

| Hang Seng | 25910.60+195.70▲ +0.76% |

| Nasdaq 100 | 24745.40-61.90▼ -0.25% |

| Nasdaq Comp | 22670.10-68.40▼ -0.30% |

| Nikkei 225 | 47672.70+670.40▲ +1.43% |

| S&P/ASX 200 | 8990.90+91.50▲ +1.03% |

| Shanghai Comp | 3912.21+44.67▲ +1.16% |

| S&P 500 E-mini | 6714.25-0.75▼ -0.01% |

| Nasdaq 100 | 24936.50+12.00▲ +0.05% |

| FTSE 100 | 9439.00-32.50▼ -0.34% |

| Euro Stoxx 50 | 5604.00-22.00▼ -0.39% |

| WTI Crude | 58.80+0.53▲ +0.91% |

| Gold | 4235.20+33.60▲ +0.80% |

| Copper | 4.95-0.06▼ -1.25% |

| US 10Y Treasury | 113.34+0.11▲ +0.10% |

| UK 10Y Gilt | 118.64-0.04▼ -0.03% |

| German 10Y Bund | 130.05-0.09▼ -0.07% |

| Italian 10Y BTP | 121.57+0.48▲ +0.40% |

| US Dollar Index | 98.37-0.04▼ -0.04% |

| VIX Volatility | 20.67-0.01▼ -0.05% |

| SONIA 3M | 96.17+0.01▲ +0.01% |

• UK GDP MoM at 07:00 BST - Forecast: 0.2% vs Previous: 0.0% - Key gauge of economic recovery momentum that could influence BoE policy stance and GBP direction.

• UK Industrial Production MoM at 07:00 BST - Forecast: 0.2% vs Previous: -0.9% - Manufacturing rebound signals could ease recession fears and support sterling if data beats expectations.

• US PPI MoM at 13:30 BST - Forecast: 0.3% vs Previous: -0.1% - Critical inflation gauge that feeds into PCE data and will shape Fed rate cut expectations ahead of next week's FOMC meeting.

• US Retail Sales MoM at 13:30 BST - Forecast: 0.4% vs Previous: 0.6% - Consumer spending strength indicator that could determine whether the Fed maintains hawkish tone or signals more dovish pivot.

• EU ECB President Lagarde Speech at 17:00 BST - Lagarde's remarks could provide clarity on ECB's policy path amid eurozone growth concerns and diverging inflation trends.

• Hygon Information Technology Co., Ltd. Class A (688041) at 13:00 BST [Pre-Market] - Est: $0.06 vs Prev: $0.04 - Chinese semiconductor earnings could signal broader tech sector resilience amid ongoing geopolitical tensions affecting global chip supply chains.

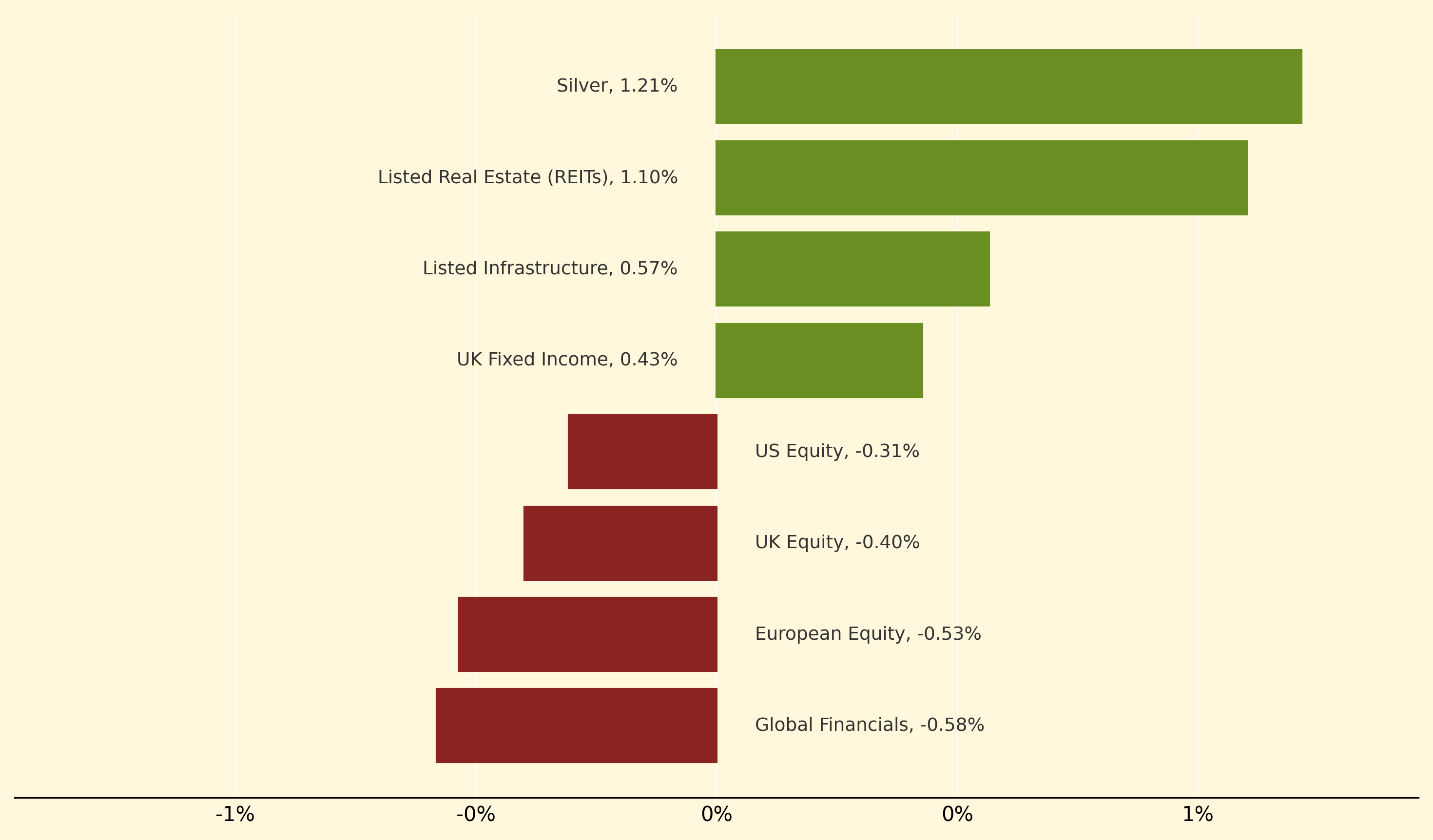

Silver led yesterday's gains, climbing 1.21% as safe-haven demand surged amid mounting US-China trade tensions over rare earth export controls. Listed Real Estate (REITs) also performed strongly, advancing 1.10%, benefiting from expectations of accelerated Fed rate cuts as policymakers connected trade uncertainty to the need for more aggressive easing.

Conversely, Global Financials underperformed significantly, dropping 0.58% despite strong US bank earnings from Morgan Stanley and Bank of America, as trade war concerns overshadowed positive fundamentals. European Equity also lagged, falling 0.53%, weighed down by geopolitical risks even as LVMH's 12.2% surge sparked an $80 billion luxury rally across the continent.

Asset class divergence: Where different categories of investments move in opposite directions simultaneously, reflecting conflicting market forces and investor sentiment about risk versus safety in uncertain economic conditions.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry