China Deploys Rare Earth Dominance in Global Supply Chain Power Play | Links: [1], [2], [3], [4], [5]

Beijing has transformed its rare earth export controls from diplomatic posturing into economic warfare, forcing carmakers across Europe and Asia to race against hard deadlines whilst Goldman Sachs quantifies the damage at $150 billion in lost global output from just a 10% supply disruption. The escalation moved from theoretical to immediate yesterday as German automakers issued production stoppage warnings and the Netherlands found itself locked in a concrete standoff with China over chipmaker Nexperia—the first major European industrial operation blocked by the new restrictions. Unlike previous broad announcements, these controls include specific compliance deadlines that companies must meet, transforming China's 80% dominance of rare earth processing from potential leverage into active economic instrument. With global renewable energy and electric vehicle production dependent on these materials, Beijing now wields $1 billion in daily export flows as bargaining power in what analysts describe as the most significant supply chain confrontation since oil embargoes of the 1970s.

BoE Governor Bailey Issues 'Alarm Bells' Warning Over Private Credit Echoing 2008 Crisis | Links: [6], [7], [8], [9], [10]

Bank of England Governor Andrew Bailey delivered his starkest warning yet about the $1.7 trillion private credit market, explicitly drawing parallels to the early stages of 2008 and announcing the first comprehensive stress testing regime targeting private equity and credit industries. Bailey specifically cited the recent collapses of First Brands and Tricolor as potential harbingers of broader systemic risks, marking the most direct regulatory challenge to shadow banking since its post-crisis expansion. "The alarm bells are ringing," Bailey told Parliament, as UK commercial real estate debt defaults soared past 20% in the latest survey data. The Governor's concerns escalated beyond previous general warnings to concrete regulatory intervention, with new stress tests designed to expose vulnerabilities in the sector that has grown from virtually nothing to nearly match traditional bank lending. This regulatory pivot comes as private credit funds face their first major test since interest rates began rising, with Bailey cautioning that current warning signs mirror those ignored in the lead-up to the global financial crisis.

Japan's Historic Female PM Takaichi Announces Major Stimulus to Combat Inflation | Links: [11], [12], [13], [14]

History was made in Tokyo as Sanae Takaichi became Japan's first female prime minister, immediately signalling a major fiscal policy shift by announcing an economic stimulus package exceeding $92 billion to tackle persistent inflation. The comprehensive package targets household inflation relief whilst heavily investing in AI and semiconductor capabilities, marking a fundamental pivot from Japan's traditionally cautious fiscal approach to addressing price pressures through aggressive government spending rather than monetary tools alone. Takaichi's appointment sent the Nikkei to fresh records as markets priced in coordinated monetary-fiscal policy that prioritises growth over currency strength, with potential new deficit bond issuance representing the most significant change in Japan's economic framework since Abenomics. Sources close to the prime minister's office indicate the stimulus will include direct cash transfers to households alongside substantial infrastructure investments, suggesting Japan is abandoning its decades-long deflationary mindset in favour of proactive inflation management through fiscal expansion. This policy revolution comes as Japan grapples with inflation above 3% for the first time in three decades.

Taiwan Export Surge Highlights AI-Driven Global Tech Recovery | Links: [15], [16]

Taiwan delivered the clearest signal yet of global technology sector recovery as export orders surged 30.5% in September, dramatically exceeding forecasts and hitting record levels on soaring artificial intelligence demand. The semiconductor-driven performance marked the strongest single-month growth since April and the most robust year-over-year increase in over 12 months, validating earlier predictions about AI infrastructure buildout accelerating globally despite ongoing US-China trade tensions. As the world's leading chip manufacturer, Taiwan's export data provides crucial real-time insights into global technology demand patterns, with the latest figures indicating that AI-driven investment is not only resilient but accelerating beyond previous expectations. The surge offers concrete validation for technology sector valuations that have been supported largely by future promises rather than current fundamentals, with Taiwan's position at the centre of global semiconductor supply chains making these export figures a leading indicator for the broader tech ecosystem's health.

Gold's 5% Plunge Signals End of Safe-Haven Rally Amid Trade Optimism | Links: [17], [18], [19], [20]

Gold crashed 5% in its steepest sell-off since 2020, with silver posting similarly dramatic losses as investors took profits from record-high positions and recalibrated portfolios amid emerging trade optimism and reduced geopolitical premium. After reaching above $4,000 per ounce with 54% year-to-date gains, the precious metals rout represents a fundamental shift in risk appetite rather than routine profit-taking, coinciding with Trump's uncertainty about direct China talks and broader risk-on sentiment across markets. Chinese mining stocks exemplified the reversal, with CNMC Goldmine tumbling after 400% gains earlier this year, whilst the London gold association's push for enhanced futures infrastructure highlights structural changes occurring in the $35 trillion London gold market alongside this historic sell-off. The sudden collapse indicates investors are pricing out significant geopolitical and inflation hedging premiums that have driven gold's relentless advance, potentially signalling renewed confidence in traditional assets and growth prospects as trade tensions show signs of easing.

| S&P 500 | 6735.35-1.40▼ -0.02% |

| FTSE 100 | 9427.00+23.40▲ +0.25% |

| CAC 40 | 8258.86+52.51▲ +0.64% |

| DAX 40 | 24330.00+19.60▲ +0.08% |

| Dow Jones | 46924.70+217.60▲ +0.47% |

| Euro Stoxx 50 | 5686.83+0.06▲ +0.00% |

| Hang Seng | 26027.60-132.60▼ -0.51% |

| Nasdaq 100 | 25127.10-12.70▼ -0.05% |

| Nasdaq Comp | 22953.70-30.90▼ -0.13% |

| Nikkei 225 | 49316.10-359.30▼ -0.72% |

| S&P/ASX 200 | 9094.70+62.80▲ +0.70% |

| Shanghai Comp | 3916.33+45.58▲ +1.18% |

| S&P 500 E-mini | 6785.25+12.00▲ +0.18% |

| Nasdaq 100 | 25318.50+23.75▲ +0.09% |

| FTSE 100 | 9462.00-3.50▼ -0.04% |

| Euro Stoxx 50 | 5683.00-17.00▼ -0.30% |

| WTI Crude | 58.29+1.05▲ +1.83% |

| Gold | 4160.10+51.00▲ +1.24% |

| Copper | 4.97+0.01▲ +0.12% |

| US 10Y Treasury | 113.73-0.02▼ -0.01% |

| UK 10Y Gilt | 118.65-0.02▼ -0.02% |

| German 10Y Bund | 130.21+0.00▲ +0.00% |

| Italian 10Y BTP | 121.80+0.23▲ +0.19% |

| US Dollar Index | 98.63-0.13▼ -0.13% |

| VIX Volatility | 19.13+0.08▲ +0.45% |

| SONIA 3M | 96.17-0.01▼ -0.01% |

• UK Inflation Rate YoY at 07:00 BST - Forecast: 4.0% vs Previous: 3.8% - Key data for Bank of England policy decisions and sterling direction as inflation remains well above target.

• UK Core Inflation Rate YoY at 07:00 BST - Forecast: 3.7% vs Previous: 3.6% - Critical measure of underlying price pressures that will influence BoE's next move on interest rates.

• UK Inflation Rate MoM at 07:00 BST - Previous: 0.3% - Provides monthly momentum reading to complement annual inflation figures for complete UK price picture.

• Indonesian Interest Rate Decision at 08:30 BST - Forecast: 4.50% vs Previous: 4.75% - Potential rate cut could signal easing cycle in emerging Asia amid global monetary policy shifts.

• South African Inflation Rate YoY at 09:00 BST - Forecast: 3.5% vs Previous: 3.3% - Rising inflation may pressure SARB to maintain hawkish stance despite economic growth concerns.

• EU ECB President Lagarde Speech at 13:25 BST - No details - Key insights into European monetary policy direction and economic outlook that could move euro and bond markets.

• Thermo Fisher Scientific Inc (TMO) at 11:00 BST [Pre-Market] - Est: $5.50 vs Prev: $5.36 - Life sciences leader's results will signal biotech sector health and lab equipment demand trends.

• Boston Scientific Corporation (BSX) at 11:30 BST [Pre-Market] - Est: $0.71 vs Prev: $0.75 - Medical device giant's performance will influence broader healthcare technology sector sentiment.

• KLA Corporation (KLAC) at 13:00 BST [Pre-Market] - Est: $8.60 vs Prev: $9.38 - Semiconductor equipment leader's results critical for chipmaker capital expenditure outlook.

• AT&T Inc. (T) at 14:30 BST [During-Hours] - Est: $0.54 vs Prev: $0.54 - Telecom giant's subscriber trends and 5G investment guidance will impact utilities and communications sectors.

• GE Vernova Inc. (GEV) at 14:30 BST [During-Hours] - Est: $1.72 vs Prev: $1.73 - Energy infrastructure spin-off's performance will influence renewable energy and industrial sectors.

• Amphenol Corporation (APH) at 14:30 BST [During-Hours] - Est: $0.79 vs Prev: $0.81 - Connector manufacturer's results will signal electronics and automotive demand strength.

• Tesla, Inc. (TSLA) at 21:00 BST [During-Hours] - Est: $0.55 vs Prev: $0.40 - EV leader's delivery guidance and autonomous driving progress will drive electric vehicle sector sentiment.

• SAP SE (SAP) at 21:05 BST [During-Hours] - Est: $1.73 vs Prev: $1.77 - Enterprise software giant's cloud transition progress will influence European tech and software sectors.

• Lam Research Corporation (LRCX) at 21:05 BST [During-Hours] - Est: $1.22 vs Prev: $1.33 - Chip equipment maker's guidance will impact semiconductor manufacturing investment outlook.

• International Business Machines Corporation (IBM) at 21:08 BST [During-Hours] - Est: $2.45 vs Prev: $2.80 - Tech veteran's AI and cloud consulting growth will influence enterprise technology transformation trends.

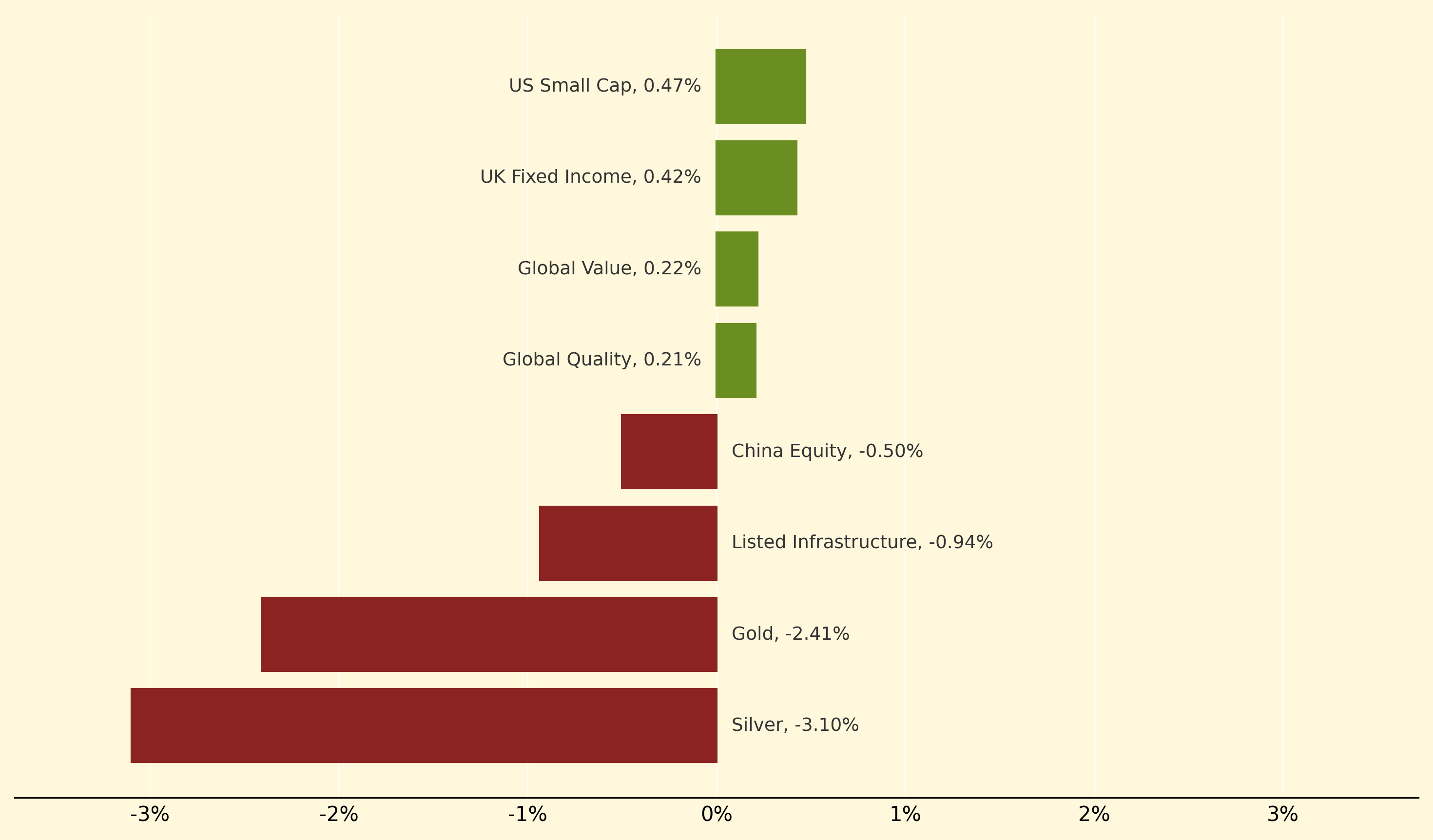

US Small Cap led gains, climbing 0.47% as domestic smaller companies benefited from reduced China trade tensions and expectations of continued Fed rate cuts supporting growth-oriented investments. UK Fixed Income also performed well, advancing 0.42% amid expectations that Bank of England policy may remain accommodative despite Bailey's private credit warnings, whilst Global Value gained 0.22% as investors rotated toward fundamentally sound assets.

Conversely, precious metals suffered dramatic losses with Silver plummeting 3.1% and Gold dropping 2.41% in their steepest sell-off since 2020, as investors took profits from record-high positions amid emerging trade optimism and reduced geopolitical hedging demand. Listed Infrastructure also lagged, falling 0.94%, whilst China Equity declined 0.5% despite Goldman Sachs' bullish long-term outlook, as rare earth export control tensions and supply chain concerns weighed on investor sentiment.

Deficit bond issuance: Government borrowing through bond markets to fund spending that exceeds current revenue, typically used during economic stimulus programmes. This debt financing mechanism allows governments to inject liquidity into economies while spreading repayment obligations across future periods, directly impacting sovereign yield curves and fiscal sustainability metrics.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry