US Sanctions Russian Oil Giants Rosneft and Lukoil, Crude Surges 3% | Links: [1], [2], [3]

The Trump administration delivered its sharpest blow yet to Putin's war machine overnight, imposing sweeping sanctions on Russia's oil giants Rosneft and Lukoil that sent crude prices surging 3% in early trading. This marks a dramatic escalation beyond previous measures that targeted trading networks and smaller entities — these new restrictions hit the core of Russia's oil production apparatus directly. Indian refiners including Reliance are scrambling to completely overhaul supply arrangements as Russian oil flows to India collapse to near-zero levels, while Chinese energy companies face similar disruptions across their supply chains. Moscow responded predictably with nuclear drills to underscore the geopolitical stakes, but the immediate market reaction suggests traders are focused on the very real supply disruptions now rippling across global energy markets.

UK Inflation Holds at 3.8%, Bank of England Rate Cut Odds Jump to 75% | Links: [4], [5], [6]

UK inflation delivered an unexpected gift to dovish Bank of England policymakers, holding steady at 3.8% for September rather than accelerating as markets had braced for. The stability represents a marked departure from the sharp upticks in July and August that consistently surprised to the upside, providing the BoE with exactly the kind of predictable trajectory it needs to consider easing. Money markets immediately jumped December rate cut probability to 75% from 50%, while two-year gilt yields slid to 14-month lows on the news. While 3.8% remains well above the central bank's 2% target, the sustained level gives policymakers breathing room ahead of Chancellor Reeves' critical Budget announcement and signals the inflation volatility that dominated summer months may be stabilising.

Foreign Investors Pour $29 Billion Into Japanese Equities Ahead of PM Vote | Links: [7], [8], [9]

Foreign investors have poured ¥5.28 trillion ($28.9 billion) year-to-date into Japanese equities, with the flows accelerating as new Prime Minister Takaichi officially takes office. The sustained appetite reflects validation of her stimulus-friendly policies now being implemented rather than merely promised, creating a self-reinforcing cycle where her dovish stance becomes official policy and foreign money responds accordingly. Bank of Japan watchers are pushing back rate hike expectations following her actual appointment, while the Nikkei maintains record highs despite trading at an attractive 22x P/E versus the Nasdaq's stretched 34x multiple. This positioning represents the culmination of a bet that began during Takaichi's campaign and is now being rewarded as policy accommodation becomes the official government line.

US Weighs New Software Export Controls on China as Tech Tensions Escalate | Links: [10], [11], [12]

The Trump administration is considering a potentially massive expansion of China export controls beyond semiconductors to encompass products made with US software, a move that could affect everything from consumer electronics to automotive systems. This represents a significant escalation from the chip-focused restrictions that have dominated headlines, extending the regulatory reach into the entire software ecosystem that underpins modern manufacturing. Asian markets retreated on the news as investors assessed the implications for global tech supply chains, while the ongoing automotive disruptions from Chinese chip supplier Nexperia—which has only resumed limited domestic sales despite Volkswagen warning of output stoppages—highlight just how vulnerable industries remain to these evolving restrictions. The software controls would mark yet another front in the technological decoupling between the world's two largest economies.

Barclays Announces £500 Million Buyback, Upgrades 2025 Guidance | Links: [13]

Barclays surprised markets with a £500 million share buyback programme and upgraded 2025 guidance following strong Q3 income performance, providing a rare dose of optimism in the UK banking sector. The announcement represents a clear vote of confidence in the bank's capital position and earnings trajectory, particularly striking given the complex backdrop of potential Bank of England rate cuts and looming fiscal policy changes from Chancellor Reeves' Budget. While other UK financial institutions navigate regulatory caution and economic uncertainty, Barclays' willingness to return significant capital to shareholders suggests management sees through current headwinds to a more profitable operating environment ahead. The move may signal broader resilience in UK banking that market valuations have not yet recognised.

| S&P 500 | 6699.40-41.94▼ -0.62% |

| FTSE 100 | 9515.00+87.90▲ +0.93% |

| CAC 40 | 8206.87-15.86▼ -0.19% |

| DAX 40 | 24151.10-145.10▼ -0.60% |

| Dow Jones | 46590.40-351.20▼ -0.75% |

| Euro Stoxx 50 | 5639.21-33.03▼ -0.58% |

| Hang Seng | 25781.80-115.80▼ -0.45% |

| Nasdaq 100 | 24879.00-214.60▼ -0.86% |

| Nasdaq Comp | 22740.40-200.40▼ -0.87% |

| Nikkei 225 | 49307.80+55.80▲ +0.11% |

| S&P/ASX 200 | 9030.00-64.70▼ -0.71% |

| Shanghai Comp | 3913.76+17.69▲ +0.45% |

| S&P 500 E-mini | 6738.50+1.50▲ +0.02% |

| Nasdaq 100 | 25055.50+16.25▲ +0.06% |

| FTSE 100 | 9551.00-5.50▼ -0.06% |

| Euro Stoxx 50 | 5643.00-3.00▼ -0.05% |

| WTI Crude | 60.68+2.18▲ +3.73% |

| Gold | 4101.00+35.60▲ +0.88% |

| Copper | 5.01+0.01▲ +0.20% |

| US 10Y Treasury | 113.72-0.08▼ -0.07% |

| UK 10Y Gilt | 118.64+0.01▲ +0.01% |

| German 10Y Bund | 130.13+0.03▲ +0.02% |

| Italian 10Y BTP | 121.76-0.04▼ -0.03% |

| US Dollar Index | 98.83+0.13▲ +0.13% |

| VIX Volatility | 19.45+0.14▲ +0.76% |

| SONIA 3M | 96.27+0.10▲ +0.10% |

• French Business Confidence at 07:45 BST - Previous: 96.0 - Key gauge of French corporate sentiment that may influence ECB policy expectations and eurozone market direction.

• UK CBI Industrial Trends Orders at 11:00 BST - Forecast: -30.0 vs Previous: -27.0 - Worsening manufacturing outlook could weigh on GBP and reinforce concerns about UK industrial weakness.

• Turkish TCMB Interest Rate Decision at 12:00 BST - Forecast: 39.5% vs Previous: 40.5% - Expected rate cut signals potential shift in Turkey's aggressive inflation-fighting stance, impacting emerging market sentiment.

• US Initial Jobless Claims at 13:30 BST - Forecast: 223K vs Previous: 218K - Rising claims could support Fed dovish expectations and influence USD strength ahead of next week's FOMC meeting.

• Canadian Retail Sales Ex Autos MoM at 13:30 BST - Forecast: 1.5% vs Previous: -1.2% - Strong rebound expected after prior decline, crucial for CAD and Bank of Canada rate path considerations.

• EU Consumer Confidence Flash at 15:00 BST - Forecast: -15.0 vs Previous: -14.9 - Slight deterioration in eurozone sentiment could pressure EUR and influence ECB dovish policy expectations.

• Japanese Inflation Rate YoY at 00:30 BST (Friday) - Previous: 2.7% - Critical for Bank of Japan policy trajectory and JPY direction as markets assess sustained inflation momentum.

• UK Gfk Consumer Confidence at 00:01 BST (Friday) - Forecast: -20.0 vs Previous: -19.0 - Weakening consumer sentiment reinforces concerns about UK economic resilience and potential BoE policy response.

• T-Mobile US, Inc. (TMUS) at 12:00 BST [Pre-Market] - Est: $2.42 vs Actual: $2.84 - Strong wireless subscriber growth and 5G momentum could boost telecom sector sentiment across global markets.

• Honeywell International Inc. (HON) at 11:00 BST [Pre-Market] - Est: $2.56 vs Actual: $2.75 - Industrial conglomerate's aerospace and building technologies performance signals broader economic health and manufacturing demand.

• Union Pacific Corporation (UNP) at 12:45 BST [Pre-Market] - Est: $2.99 vs Actual: $3.03 - Rail freight volumes and pricing power indicate supply chain health and economic activity levels across key US trade routes.

• Blackstone Inc. (BX) at 14:30 BST [During-Hours] - Est: $1.23 vs Actual: $1.21 - Private equity giant's results reflect credit market conditions and institutional investor appetite for alternative investments.

• Intel Corporation (INTC) at 21:01 BST [During-Hours] - Est: $0.01 vs Actual: $-0.10 - Semiconductor recovery timeline and AI chip competition will impact broader tech sector and global chip supply dynamics.

• Newmont Corporation (NEM) at 21:05 BST [During-Hours] - Est: $1.43 vs Actual: $1.43 - Gold production costs and guidance amid inflationary pressures could influence precious metals and mining sector positioning.

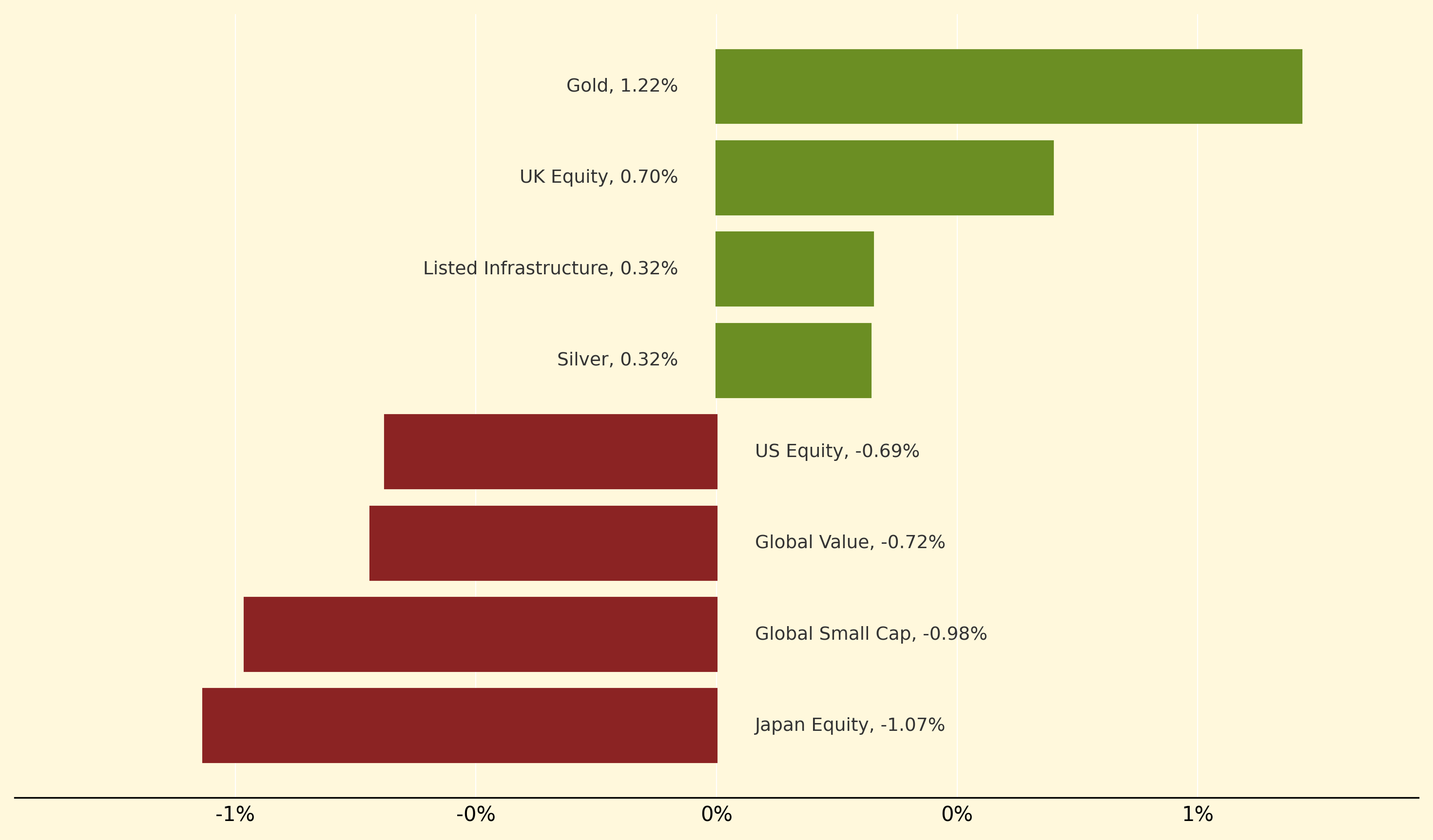

Gold led precious metals higher with a 1.22% gain as geopolitical tensions from US sanctions on Russian oil giants Rosneft and Lukoil drove safe-haven demand, while crude's 3% surge reinforced the commodity rally. UK Equity advanced 0.7% amid expectations of Bank of England rate cuts after inflation held steady at 3.8%, with money markets pricing in 75% odds of December easing following the surprisingly stable reading.

Conversely, Japan Equity dropped 1.07% despite record foreign inflows of $29 billion year-to-date, as investors took profits following Prime Minister Takaichi's official appointment and pushed back BOJ rate hike expectations. Global Small Cap fell 0.98% while US Equity declined 0.69%, both pressured by renewed US-China trade tensions as the administration considers expanding software export controls beyond semiconductors to encompass products made with US technology.

Dovish stance: A monetary policy approach where central bankers favour lower interest rates and accommodative measures to stimulate economic growth, typically signalling readiness to ease rather than tighten financial conditions when facing economic uncertainty.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry